Refinancing is defined as replacing your existing mortgage with a new loan that carries different terms, including a revised interest rate, a new repayment timeline, and sometimes a different loan type entirely. This structural reset is why refinancing improves loan structure in ways that go far beyond simply cutting your monthly payment. The real benefits show up in how your loan amortizes, how quickly you build equity, and how well your debt profile fits your financial goals. Understanding these mechanics gives you the clarity to decide whether refinancing is the right move for your situation.

Why refinancing improves loan structure through rate and term changes

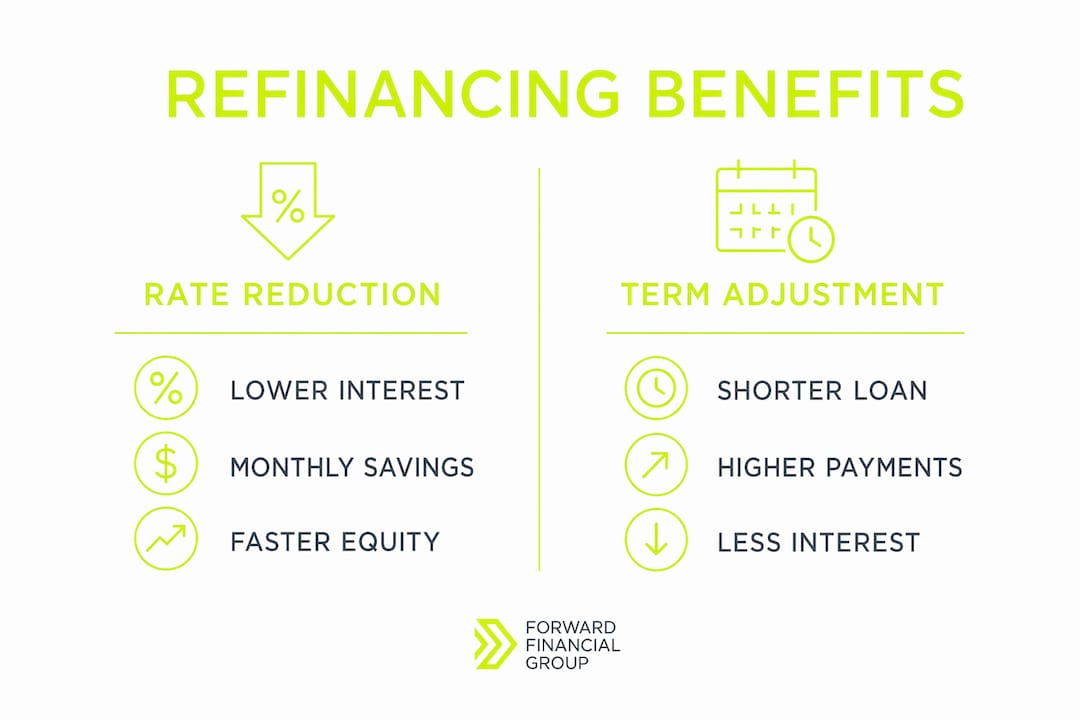

Refinancing replaces your original mortgage with a new one that can change the interest rate, the loan term, and the loan type at the same time. Each of those changes reshapes your loan's structure in a distinct way. Together, they determine how much you pay each month, how much goes to interest versus principal, and how long you carry the debt.

How interest rate changes affect your loan

Lowering your interest rate reduces the total cost of borrowing. A lower rate means less of each payment goes to the lender as interest, and more goes toward paying down your actual balance. Over a 30-year loan, even a one-point rate reduction compounds into tens of thousands of dollars in savings.

Switching between fixed and adjustable-rate mortgages through refinancing adds another layer of control. A fixed rate gives you payment predictability for the life of the loan. An adjustable-rate mortgage (ARM) can offer a lower starting rate if you plan to sell or refinance again within a few years.

How loan term changes reshape your obligations

Shortening your loan term from 30 years to 15 years raises your monthly payment but cuts your total interest dramatically. A 15-year fixed-rate mortgage forces faster principal paydown, which builds equity at a much faster pace. Extending your term does the opposite: it lowers monthly payments but increases the total interest you pay over time.

Scenario | Monthly Payment | Total Interest Paid | Equity Speed |

|---|---|---|---|

30-year at 7.0% on $300,000 | ~$1,996 | ~$418,527 | Slow |

15-year at 6.5% on $300,000 | ~$2,613 | ~$170,342 | Fast |

30-year at 5.5% (refi) on $300,000 | ~$1,703 | ~$313,212 | Moderate |

Pro Tip: Run the numbers on both a shorter term and a lower rate before committing. Sometimes a 20-year term at a lower rate beats both extremes on total cost.

How refinancing shifts your payment mix to build equity faster

Mortgage payments are split between principal and interest, and that split changes over the life of the loan. Early in a 30-year mortgage, the vast majority of each payment goes to interest. Lower interest rates shift payments toward principal earlier, which accelerates equity building in a way that a simple payment reduction does not.

This effect is most visible when you refinance in the first decade of a loan. At that stage, your amortization schedule is still heavily weighted toward interest. Refinancing to a lower rate at that point resets the schedule in your favor.

The FHA Streamline Refinance program makes this principle a formal requirement. FHA Streamline Refinance mandates a net tangible benefit, meaning the new loan must reduce your combined interest and mortgage insurance rate by at least 0.5%. That rule exists because a refinancing that does not improve your financial position is not a structural improvement at all.

Loan Year | Payment to Interest (7%) | Payment to Interest (5.5%) | Equity Gain Difference |

|---|---|---|---|

Year 1 | ~82% | ~76% | +6% toward principal |

Year 5 | ~79% | ~72% | +7% toward principal |

Year 10 | ~73% | ~64% | +9% toward principal |

Refinancing revises contract terms beyond just lowering payments. It affects affordability and borrower risk, making structural changes fundamental to long-term financial health.

How refinancing restructures debt and improves cash flow

Refinancing does more than adjust your primary mortgage. Cash-out refinancing lets you access the equity you have built and use it to consolidate higher-interest debt, fund home improvements, or cover major expenses. Q1 2026 equity withdrawals rose 2% year over year with significant second-lien lending, showing that homeowners are actively using their home equity as a financial tool.

Second-lien loans, such as home equity lines of credit, allow you to access equity while preserving a low-rate first mortgage. This approach restructures your debt profile without disturbing the favorable terms on your primary loan. The result is a layered debt structure that can improve monthly cash flow without sacrificing the rate you locked in years ago.

The key benefits of refinancing for debt restructuring include:

Lower debt-to-income ratio: Consolidating high-interest debt into a lower-rate mortgage reduces your monthly obligations relative to income.

Improved cash flow: Reducing total monthly debt payments frees up money for savings, investments, or other financial goals.

Equity access without selling: Cash-out refinancing gives you liquidity without requiring you to sell your home.

Debt consolidation: Rolling credit card or personal loan balances into a mortgage rate that is significantly lower cuts your overall interest burden.

Cash-out refinancing and second liens alter your debt profile and equity access in ways that require careful planning. The structural benefit is real, but it depends on using the accessed equity productively rather than adding to consumer debt.

Common pitfalls when refinancing for loan structure improvement

Refinancing is not automatically beneficial. Lowering monthly payments by extending your loan term can increase the total interest you pay over the life of the loan. A homeowner who refinances a 25-year remaining balance into a new 30-year loan saves money each month but adds five years of interest payments.

Closing costs are the second major factor. Refinancing involves costs like closing fees and credit checks, which must be offset by long-term savings before the transaction delivers real value. The break-even point is the number of months it takes for your monthly savings to cover those upfront costs.

Calculate your break-even point. Divide total closing costs by your monthly savings. If the result is 36 months and you plan to move in two years, refinancing does not improve your financial position.

Check your loan payoff horizon. Refinancing into a longer term resets your amortization clock. Confirm the new payoff date aligns with your financial plans.

Verify the net tangible benefit. Refinancing is justified only when benefits outweigh closing costs and do not simply extend the loan term without financial gain.

Review your credit score first. A lower credit score at the time of refinancing can result in a higher rate than expected, reducing or eliminating the structural benefit.

Account for mortgage insurance changes. Switching loan types can add or remove private mortgage insurance, which affects your true monthly cost.

Pro Tip: Ask your lender for a side-by-side amortization comparison of your current loan and the proposed refinanced loan. The total interest column tells the real story.

How to decide if refinancing will truly improve your loan structure

A sound refinancing decision requires evaluating several factors at the same time. Effective refinancing creates improved repayment conditions after costs and risks, not just a lower monthly payment. The following steps give you a practical framework.

Check current market rates. Compare today's rates against your existing rate using the current mortgage rates page to see if a meaningful reduction is available.

Use a refinance calculator. A refinance savings calculator shows your break-even point, monthly savings, and total interest impact in one view.

Review your loan type. Determine whether switching from an ARM to a fixed rate, or from an FHA loan to a conventional loan, improves your long-term cost structure.

Assess your equity position. You need sufficient equity to qualify for favorable terms and to make cash-out refinancing viable without adding mortgage insurance.

Consult a mortgage professional. A broker who specializes in refinancing can compare multiple lenders and identify options that match your specific financial goals.

Evaluating a refinance requires balancing cash flow benefits against total interest and loan amortization timelines. No single metric tells the full story. The combination of rate, term, closing costs, and your remaining loan balance determines whether the structural change is genuinely beneficial.

Key Takeaways

Refinancing improves loan structure by resetting your interest rate, loan term, and payment allocation to reduce total borrowing costs and build equity faster.

Point | Details |

|---|---|

Rate reduction shifts payment mix | Lower rates direct more of each payment toward principal, accelerating equity growth. |

Term changes carry trade-offs | Shorter terms cut total interest; longer terms lower payments but cost more overall. |

Break-even analysis is required | Divide closing costs by monthly savings to confirm refinancing delivers net financial gain. |

Cash-out refinancing restructures debt | Accessing equity can consolidate high-interest debt and improve monthly cash flow. |

Net tangible benefit must be confirmed | FHA Streamline rules require at least a 0.5% rate reduction, a useful benchmark for all refinances. |

What I have learned counseling homeowners through refinancing decisions

Most homeowners come to me focused on one number: the monthly payment. That focus is understandable, but it misses the larger picture. The monthly payment is a symptom of your loan structure. The structure itself is what determines your financial outcome over 15 or 30 years.

The clients who benefit most from refinancing are the ones who ask the right questions before signing. They want to know how the new loan affects their total interest, their equity position in five years, and their payoff date. Those three questions reveal whether a refinancing is a genuine structural improvement or just a short-term cash flow fix.

The mistake I see most often is refinancing into a longer term to lower a payment without running the total interest comparison. A homeowner with 22 years left on a mortgage who refinances into a new 30-year loan has just added eight years of payments. The monthly savings rarely justify that cost when you look at the full picture.

Closing costs deserve the same scrutiny. A refinancing that costs $6,000 upfront and saves $150 per month takes 40 months to break even. If there is any chance you will sell or refinance again before that point, the transaction does not improve your loan structure. It just adds cost.

My advice is to treat refinancing as a financial decision, not a rate-chasing exercise. The goal is a loan structure that fits your life plan, builds equity efficiently, and reduces your total cost of borrowing. When those three conditions are met, refinancing is one of the most powerful tools available to a homeowner.

— David Mordue

How David Mordue - Forward Financial Group can help you refinance with confidence

Knowing the theory behind loan restructuring is one thing. Seeing the numbers applied to your specific mortgage is another.

David Mordue - Forward Financial Group offers a fully online refinancing process with funding in less than 21 days. You can use the refinance calculator to estimate your break-even point, monthly savings, and total interest impact before speaking with anyone. When you are ready for a personalized rate comparison, the mortgage refinance service connects you with expert guidance tailored to your loan balance, credit profile, and financial goals. Clients consistently report significant monthly savings after working with David Mordue - Forward Financial Group on their refinancing decisions.

FAQ

What does refinancing do to your loan structure?

Refinancing replaces your existing mortgage with a new loan that can change the interest rate, loan term, and loan type. These changes alter your amortization schedule, monthly payment, and total interest paid.

When does refinancing actually improve your financial position?

Refinancing improves your position when the long-term savings exceed the upfront closing costs and the new loan does not simply extend your repayment timeline without financial gain.

How does refinancing affect equity building?

Lower interest rates shift more of each payment toward principal earlier in the loan, which builds home equity faster than a higher-rate loan with the same term.

What is the break-even point in refinancing?

The break-even point is the number of months it takes for your monthly savings to cover your closing costs. Divide total closing costs by your monthly savings to calculate it.

Is cash-out refinancing a good way to restructure debt?

Cash-out refinancing can consolidate high-interest debt into a lower mortgage rate, improving monthly cash flow. The benefit depends on using the equity productively and not extending your loan term unnecessarily.

Recommended

David Mordue - Get Your Mortgage Pre-Approval or Mortgage Refinance Today

David Mordue - Get Your Mortgage Pre-Approval or Mortgage Refinance Today