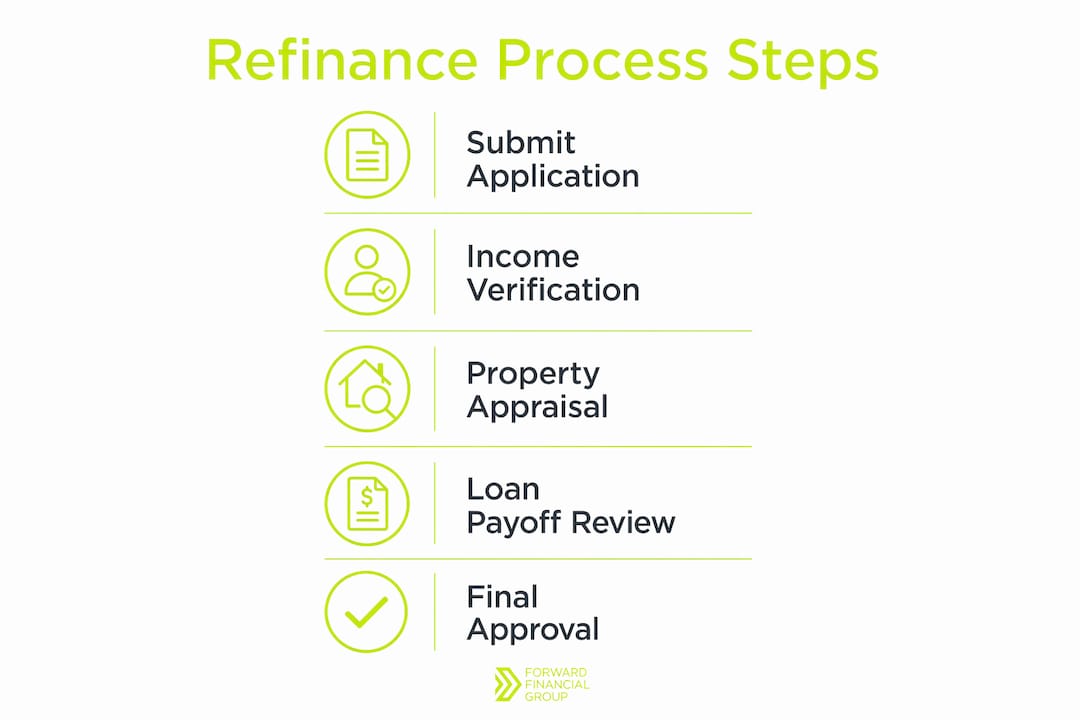

Refinancing is defined as replacing your existing mortgage with a completely new loan, and lenders treat it as a fresh risk event requiring full underwriting from scratch. That distinction is the foundation of why lenders value refinance applications. Every refinance triggers updated verification of your credit score, debt-to-income ratio (DTI), loan-to-value ratio (LTV), and current property value. Understanding what lenders check and why gives you a real advantage when you apply, whether you are pursuing a lower rate, a shorter term, or a better loan structure.

Why lenders value refinance applications: the core reason

Refinancing creates new lending riskbecause the lender is issuing a brand-new loan, not extending the old one. Your financial situation may have changed since you first borrowed. Your income, credit, and home value could all look different today than they did at closing.

Lenders must confirm that the new loan is properly supported before they commit capital. That means verifying your current ability to repay and confirming that the property can secure the new loan amount. A lender who skips this step takes on risk that investors who purchase mortgage-backed securities will not accept.

This is also why the importance of refinance applications goes beyond paperwork. The application triggers a full review cycle that protects both sides. You get a loan you can actually afford at terms that reflect your real financial position. The lender gets a loan that meets investor standards and regulatory requirements.

What do lenders verify in refinance applications and why?

Lenders re-check three core areas in every refinance: borrower qualification, property value, and the existing loan payoff. Each area carries its own risk, and a problem in any one of them can stop approval.

Borrower qualification: credit, income, and DTI

Credit score signals default risk, DTI measures whether your income supports the new payment, and LTV shows how much equity cushions the lender against loss. These three metrics work together, not in isolation. Fannie Mae's Desktop Underwriter, for example, weighs the combined picture rather than applying rigid cutoffs to each number individually. A strong cash reserve or a clean payment history can compensate for a DTI that sits slightly above the standard threshold.

Property value and LTV

Mortgage lenders require appraisalsto estimate current market value, which determines the LTV ratio. LTV is the percentage of the home's value covered by the loan. A lower LTV means more equity, which reduces lender risk and often unlocks better rates. If your home has declined in value since your original purchase, your LTV rises and your refinance options narrow.

Existing loan payoff and title verification

The lender must calculate an exact payoff amount for your current mortgage and verify that no liens or title issues exist. A refinance file can fail after application due to payoff inaccuracies or title problems that were invisible at the rate quote stage. These issues do not show up until the underwriting process begins, which is why thorough preparation matters before you submit.

Pro Tip: Gather your most recent mortgage statement, two years of tax returns, recent pay stubs, and a list of all debts before you apply. Complete documentation cuts underwriting cycles and speeds your closing.

How do refinance program rules shape lender requirements?

Structured refinance programs add another layer to how lenders assess refinancing. Each program carries specific eligibility rules, and the application is how lenders confirm you qualify.

Freddie Mac's Refi Possible program is a clear example. Refi Possible requires a minimum 50 basis point rate reduction and a total monthly payment decrease. The program caps LTV at 97%, limits cash access at closing to $250, and requires sufficient credit history without setting a hard minimum credit score. These rules exist to confirm that the refinance delivers a real financial benefit to the borrower, not just a new loan.

Lenders use the application to document that your loan meets these benefit tests. If the numbers do not clear the thresholds, the program does not apply and the lender must route you through traditional underwriting instead. That distinction affects your timeline, your documentation requirements, and your final rate.

Criteria | Refi Possible (Freddie Mac) | Traditional refinance |

|---|---|---|

Minimum rate reduction | 50 basis points | None required |

Maximum LTV | 97% | Typically 80–97% |

Cash out at closing | $250 maximum | Up to program limits |

Credit score minimum | No hard minimum | Usually 620+ |

Payment benefit required | Yes, total payment must decrease | Not required |

Underwriting path | Streamlined if tests pass | Full traditional underwriting |

Pro Tip: Ask your mortgage broker to run your numbers through both streamlined and traditional underwriting paths before you commit to a program. The faster path is not always the cheaper one.

Knowing which program you qualify for is one of the most practical reasons to refinance loans with a broker who understands program compliance. The wrong program choice adds weeks to your timeline and can cost you a better rate.

Why refinance applications reflect mortgage market activity

Refinance applications are not just individual transactions. They are a real-time signal of market conditions, and lenders watch application volume closely to manage capacity and pricing.

The Mortgage Bankers Association reported that refinance app volume rose 15% week-over-week, reaching 40.2% of all mortgage applications in june 2026. Total mortgage applications rose 10.8% during the same period, with the 30-year fixed rate sitting at 6.6%. That volume shift tells lenders that borrower demand is real and that rate conditions are favorable enough to trigger action.

High refinance volume affects lenders in several direct ways:

Capacity pressure: Lenders must staff underwriting and processing teams to match application flow. Surges in volume can extend timelines if lenders are not prepared.

Investor demand: Mortgage-backed securities investors absorb refinanced loans. Strong investor appetite supports competitive rates and broader loan availability.

Pricing strategy: When refinance volume rises, lenders sometimes adjust pricing to manage pipeline risk and protect margins.

Rate sensitivity: Refinance borrowers are more rate-sensitive than purchase borrowers. A small rate drop can trigger a large application spike, which lenders must anticipate.

Understanding these market dynamics helps you time your application. Submitting when volume is moderate often means faster processing and more lender attention to your file.

Common pitfalls homeowners should avoid in refinance applications

Refinance applications fail for reasons that have nothing to do with your credit score. Most failures come from preparation gaps that surface during underwriting.

Inaccurate payoff amounts. Your current lender's payoff figure changes daily due to interest accrual. Using an outdated number creates a cash-to-close discrepancy that can delay or kill your closing.

Title issues. Unpaid contractor liens, unresolved judgments, or errors in public records can block title transfer. Order a preliminary title report early so you have time to resolve problems.

Incomplete or outdated documentation. Lenders require documents dated within 30 to 60 days of closing. A pay stub from three months ago will not clear underwriting. Refresh your documents right before submission.

Misunderstanding benefit thresholds. Programs like Refi Possible require documented payment decreases. If your new rate does not clear the minimum reduction test, you lose access to streamlined processing and may face a longer approval path.

Ignoring cash-to-close requirements. Even a no-cash-out refinance has closing costs. Failing to account for these upfront leads to last-minute surprises that delay funding.

Prompt, thorough application completion reduces avoidable underwriting cycles. Every round trip between you and the underwriter adds days to your timeline and increases the chance that a rate lock expires.

Pro Tip: Request your official mortgage payoff statement the week you plan to submit your application. Use that figure, not your online balance, when calculating cash to close.

Key takeaways

Lenders value refinance applications because they create a structured, documented process that protects both the borrower and the lender from the risks of issuing a new loan without current financial verification.

Point | Details |

|---|---|

Refinancing is a new loan | Lenders treat every refinance as a fresh risk event requiring full underwriting, not a simple extension. |

Three metrics drive approval | Credit score, DTI, and LTV are re-verified together; compensating factors can offset borderline numbers. |

Program rules add eligibility tests | Programs like Freddie Mac's Refi Possible require documented rate and payment reductions to qualify for streamlined processing. |

Market volume signals matter | Refinance applications comprised 40.2% of all mortgage applications in june 2026, directly influencing lender capacity and pricing. |

Preparation prevents failure | Payoff accuracy, current documentation, and title verification are the most common failure points in refinance underwriting. |

What I have learned from watching refinance applications succeed and fail

After working with homeowners across a wide range of financial situations, I have come to see the refinance application process differently than most people expect. Homeowners often treat it as a formality, a box to check before getting a lower rate. That mindset is the single biggest reason applications stall.

The verification process exists because your financial life has moved since you first closed. Your income may be higher or lower. Your home may have appreciated or pulled back. Your debt load may have shifted. Automated underwriting systems like Fannie Mae's Desktop Underwriter are sophisticated enough to weigh all of these factors together, which means a borderline DTI does not automatically disqualify you if your reserves and payment history are strong.

What I tell every homeowner is this: the application is your opportunity, not your obstacle. A thorough, well-prepared file moves faster, attracts better lender attention, and gives you more negotiating room on rate and terms. Rushing it or submitting incomplete documents hands the lender a reason to slow down.

The homeowners I have seen get the best outcomes treat the refinance as a fresh financial review. They pull their credit reports in advance, resolve any errors, and know their DTI before the lender calculates it. They choose their program based on documented benefit, not just the lowest rate advertised. That preparation is what separates a 21-day closing from a 60-day ordeal.

— David Mordue

How David Mordue - Forward Financial Group can support your refinance

Knowing what lenders look for is the first step. Putting that knowledge to work in your specific situation is where professional guidance makes a real difference.

David Mordue - Forward Financial Group offers a fully online refinance process with funding possible in under 21 days. You can use the refinance savings calculator to estimate your potential monthly savings and check whether your numbers clear common program thresholds before you apply. When you are ready to move forward, the mortgage refinance service connects you with personalized rate comparisons and expert support through every step of underwriting. Clients have reported significant monthly savings through competitive rates and a process built around their specific financial goals.

FAQ

What is the main reason lenders require a refinance application?

Lenders require a refinance application because refinancing creates a new loan, not an extension of the old one. Updated borrower qualification, property appraisal, and title verification are required before any new funds are committed.

Which financial metrics do lenders check most closely in a refinance?

Lenders re-verify credit score, debt-to-income ratio, and loan-to-value ratio on every refinance. Automated underwriting tools like Fannie Mae's Desktop Underwriter evaluate these together, so strong compensating factors can offset a single borderline metric.

Do all refinance programs have the same eligibility rules?

No. Programs like Freddie Mac's Refi Possible carry specific tests, including a minimum 50 basis point rate reduction and a required total payment decrease. Traditional refinances do not require documented benefit thresholds.

How does a home appraisal affect my refinance approval?

The appraisal sets your home's current market value, which determines your LTV ratio. A lower LTV gives the lender more security and typically unlocks better rates and broader program eligibility.

What is the fastest way to avoid delays in refinance underwriting?

Submit complete, current documentation from the start and use an official payoff statement dated within the week of your application. Thorough, timely file completion eliminates the most common causes of underwriting delays.