A mortgage is defined as a secured loan used to purchase or refinance real estate, with the property itself serving as collateral to guarantee repayment. Most mortgage loans run for 15 to 30 years, and borrowers repay the debt in fixed monthly installments that cover both principal and interest. The Consumer Financial Protection Bureau (CFPB) and Freddie Mac both publish standards that govern how lenders structure and disclose these loans. Understanding mortgage basics before you apply puts you in a stronger position to choose the right loan, negotiate better terms, and avoid costly surprises at closing.

What is a mortgage and how does it work?

A mortgage loan functions as an installment debt, meaning you borrow a lump sum and repay it monthly over the agreed term. Each payment chips away at the principal (the original amount borrowed) while also covering the interest the lender charges for extending credit. This repayment structure is called amortization. Early payments are weighted heavily toward interest, while later payments shift toward reducing the principal balance.

The property you buy secures the loan. That security gives the lender a legal right to act if you stop paying. Specifically, lenders can foreclose and sell the property if you fail to meet payment obligations or violate loan conditions such as maintaining homeowners insurance. Foreclosure is the lender's primary protection against default. This is what separates a mortgage from an unsecured personal loan, where no collateral backs the debt.

Here is what makes a mortgage different from other borrowing:

Collateral required. The home secures the loan, which lowers the lender's risk and typically results in lower interest rates than unsecured debt.

Long repayment term. Terms of 15 or 30 years spread payments over time, making large purchase prices manageable.

Amortization schedule. Each payment is calculated so the loan reaches a zero balance exactly at the end of the term.

Foreclosure risk. Missing payments can trigger a legal process that results in losing the home.

Pro Tip: Request a full amortization schedule from your lender before signing. Seeing exactly how much interest you will pay over the life of the loan often motivates borrowers to make extra principal payments early, which can save thousands of dollars.

What are the main types of mortgages?

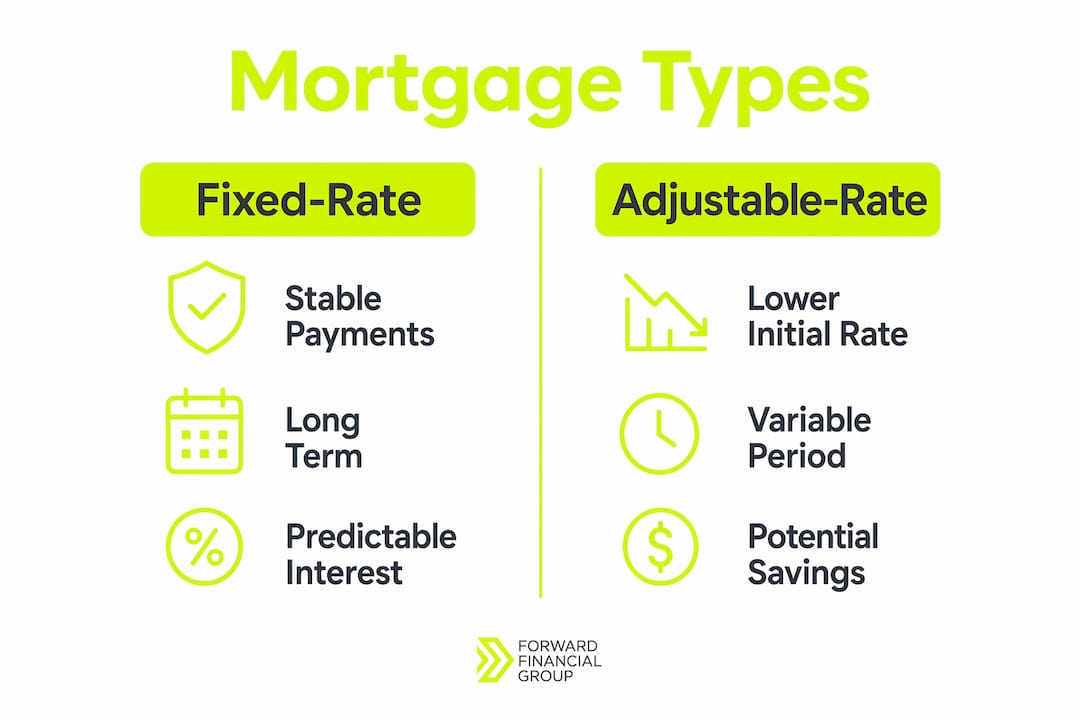

The CFPB identifies two primary rate structures: fixed-rate mortgages and adjustable-rate mortgages (ARMs). Each suits a different financial situation and ownership timeline.

Fixed-rate mortgages

A fixed-rate mortgage locks your interest rate for the entire loan term. Your principal and interest payment never changes, which makes budgeting straightforward. A 30-year fixed-rate mortgage offers the lowest monthly payment but the highest total interest cost. A 15-year fixed-rate mortgage costs more per month but builds equity faster and carries significantly less total interest.

Adjustable-rate mortgages

An adjustable-rate mortgage starts with a lower rate for a set introductory period, typically 5, 7, or 10 years, then adjusts periodically based on a market index. ARMs work well for buyers who plan to sell or refinance before the adjustment period begins. They carry more risk for buyers who stay long-term, since rates can rise substantially after the fixed period ends.

Government-backed loan programs

Freddie Mac notesthat government-backed programs such as FHA, VA, and jumbo loans serve distinct borrower profiles with different eligibility rules and benefits.

Loan type | Best for | Key benefit |

|---|---|---|

FHA loan | First-time buyers, lower credit scores | Low down payment requirement |

VA loan | Eligible veterans and service members | No down payment, no PMI |

Jumbo loan | High-value property purchases | Finances amounts above conforming limits |

Conventional | Strong credit, standard purchase | Flexible terms, no upfront fees |

FHA loansare particularly popular with first-time buyers because they accept lower credit scores and smaller down payments than conventional loans.VA loansoffer the most favorable terms available, but eligibility is limited to qualifying military borrowers.

Pro Tip: The CFPB recommends matching your loan type to your planned ownership timeline. If you expect to stay in the home for more than seven years, a fixed-rate loan almost always delivers better long-term value than an ARM.

What does the mortgage application process involve?

The homebuying process follows a defined sequence from pre-approval through closing, with closing typically taking 30–45 days from application to funding. Knowing each step reduces stress and helps you avoid delays.

Get pre-approved. A lender reviews your income, assets, credit score, and debt to issue a pre-approval letter. This letter tells sellers you are a serious buyer and gives you a clear budget.

Search for a home. With a pre-approval in hand, you shop within your confirmed price range and make an offer on a property.

Submit your mortgage application. Once the seller accepts your offer, you formally apply for the loan and provide full documentation including tax returns, pay stubs, and bank statements.

Go through underwriting. The lender's underwriter verifies every detail of your application, orders an appraisal, and confirms the property meets loan requirements.

Respond to stipulations. Underwriters frequently request additional documents during review. Responding quickly keeps your closing on schedule.

Close on the loan. You sign final documents, pay closing costs, and the lender funds the loan. You receive the keys.

Unexpected documentation requests during underwriting, sometimes called "stipulations," can delay closing by several days and put the scheduled funding date at risk. Buyers who prepare their financial documents in advance consistently experience fewer delays. Keeping two years of tax returns, recent pay stubs, and three months of bank statements ready before you apply is the single most effective way to protect your timeline.

Pro Tip: Avoid making large purchases, opening new credit accounts, or changing jobs between pre-approval and closing. Any of these actions can trigger a re-review of your file and delay funding.

What components make up your monthly mortgage payment?

A mortgage payment covers more than just the loan balance and interest. Freddie Mac confirms that a full mortgage payment typically includes principal, interest, escrow for taxes and insurance, and sometimes private mortgage insurance and HOA fees.

Understanding each component helps you calculate your true monthly cost before you commit to a purchase price.

Principal. The portion of your payment that reduces the loan balance. This grows larger with each passing year as amortization shifts the payment structure.

Interest. The lender's fee for extending the loan. Expressed as an annual percentage rate (APR), it determines how much you pay above the original loan amount.

Property taxes. Most lenders collect a monthly portion of your annual property tax bill and hold it in an escrow account, then pay the tax authority directly.

Homeowners insurance. Lenders require coverage to protect the collateral. This premium is also typically escrowed and paid on your behalf.

Private mortgage insurance (PMI). Required on conventional loans when your down payment is below 20%. PMI protects the lender, not you, and can be removed once you reach 20% equity.

HOA fees. If your property belongs to a homeowners association, monthly dues may be factored into your total housing cost, though they are usually paid separately.

Payment component | Who it protects | When it applies |

|---|---|---|

Principal + interest | Lender (loan repayment) | Every month |

Property taxes (escrowed) | Local government | Every month via escrow |

Homeowners insurance | Lender and homeowner | Every month via escrow |

PMI | Lender only | Until 20% equity reached |

HOA fees | Community association | Monthly if applicable |

Key Takeaways

A mortgage is a secured real estate loan repaid in monthly installments over 15–30 years, and choosing the right loan type, understanding all payment components, and preparing documents in advance are the three factors that most determine your success as a borrower.

Point | Details |

|---|---|

Mortgage definition | A secured loan backed by real estate, repaid monthly over 15–30 years. |

Loan types matter | Fixed-rate suits long-term owners; ARMs suit buyers who plan to move or refinance within a few years. |

Full payment picture | Monthly costs include principal, interest, taxes, insurance, and possibly PMI or HOA fees. |

Process preparation | Organizing financial documents before applying reduces underwriting delays and protects your closing date. |

Government programs | FHA, VA, and jumbo loans serve specific borrower profiles with distinct eligibility rules and benefits. |

What I have learned from working with mortgage borrowers every day

The single biggest mistake I see borrowers make is treating the mortgage process as something that happens to them rather than something they actively manage. Buyers who show up to pre-approval with disorganized paperwork, or who make a large purchase on credit between application and closing, consistently face delays and sometimes lose the home they wanted.

The second thing I have noticed is that most first-time buyers default to a 30-year fixed loan without ever running the numbers on a 15-year term. The monthly payment is higher, but the total interest savings over the life of the loan can be substantial. For buyers who can afford the difference, the 15-year option deserves serious consideration.

On loan type selection, I have seen buyers choose an ARM because the initial rate looked attractive, without fully accounting for how long they actually planned to stay in the home. The CFPB's guidance on this is sound: match your loan structure to your realistic ownership timeline, not your optimistic one. If there is any chance you will be in the home for more than seven years, a fixed rate gives you certainty that an ARM cannot.

My strongest advice is to communicate proactively with your lender throughout the process. When underwriting sends a stipulation request, respond the same day. Every day of delay at that stage risks your closing date and, in competitive markets, can cost you the deal entirely.

— David Mordue

Ready to take your next step with confidence?

Knowing the mortgage basics is the foundation. Putting that knowledge into action with the right loan and the right rate is where real financial progress happens.

David Mordue - Forward Financial Group offers a fully online application process with funding possible in less than 21 days. Whether you are buying your first home or exploring refinancing to reduce your monthly payment, the team provides personalized rate comparisons and expert guidance at every stage. Use the refinance savings calculator to see what a lower rate could mean for your budget, or check the rent vs. buy tool to confirm homeownership makes financial sense for your situation. When you are ready to move forward, get your pre-approval and lock in your rate with a team that prioritizes your timeline.

FAQ

What is a mortgage loan in simple terms?

A mortgage loan is money borrowed from a lender to buy or refinance a home, with the property serving as collateral. You repay the loan in monthly installments over a set term, typically 15 or 30 years.

How does a mortgage differ from a regular loan?

A mortgage is secured by real estate, which gives the lender the right to foreclose and sell the property if you default. An unsecured personal loan carries no collateral, which is why mortgage rates are generally lower.

What credit score do I need to qualify for a mortgage?

Conventional loans typically require a credit score of 620 or higher, while FHA loans may accept lower scores. VA loans have no official minimum score set by the government, though individual lenders apply their own standards.

How long does the mortgage application process take?

The process from application to closing typically takes 30–45 days. Delays most often occur during underwriting when additional documentation is requested.

What is PMI and can I avoid it?

Private mortgage insurance (PMI) is required on conventional loans when your down payment is below 20%. You can avoid it by putting 20% down, or you can request its removal once your equity reaches that threshold.