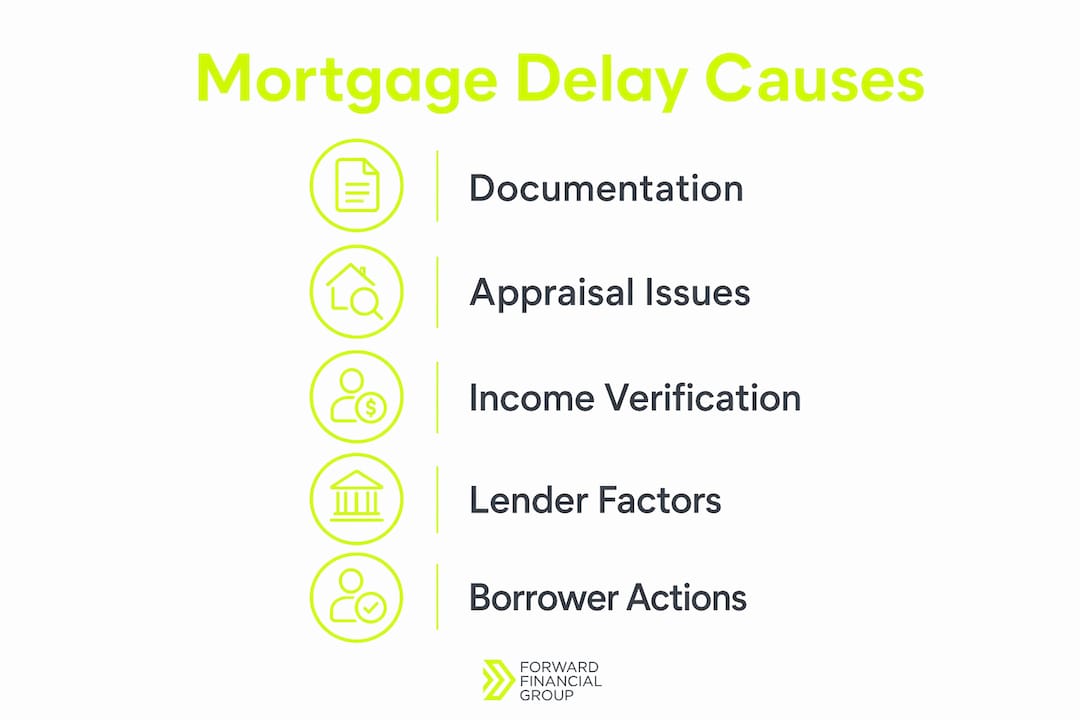

Mortgage approval delays are defined as any extension of the standard underwriting timeline caused by incomplete documentation, appraisal complications, income verification issues, or lender processing backlogs. The full approval process typically runs 42 to 50 days from application to closing, with underwriting consuming the largest share of that time. Most delays are not random. They follow predictable patterns that borrowers can prepare for once they understand the causes. This guide explains why delays occur in mortgage approval and what you can do to keep your timeline on track.

Why delays occur in mortgage approval: documentation problems

Documentation issues are the single most common cause of mortgage approval delays. Lenders require a complete, current, and legible paper trail before an underwriter can make a decision. A single missing page from a bank statement or a blurry copy of a tax return is enough to pause the entire review.

The standard document package a lender requests includes:

Pay stubs from the last 30 days

W-2 forms from the past two years

Federal tax returns from the past two years

Bank statements from the past two to three months

Government-issued photo ID

Proof of assets such as investment or retirement account statements

Each of these documents must be complete. Lenders reject partial submissions and request resubmission, which restarts the clock on that portion of the review. Pre-approvals typically take 1–3 days, but delays beyond a week almost always trace back to missing documents, credit disputes, or lender backlogs.

Credit disputes add another layer of complexity. When a borrower has an active dispute on their credit report, many lenders cannot finalize the credit review until the dispute is resolved. That resolution can take weeks if it involves a creditor or the credit bureaus.

Self-employed borrowers face a longer documentation process by default. Rather than submitting simple pay stubs, self-employed applicants require multi-year tax reviews that examine business income, deductions, and net profit trends. This adds meaningful time to the underwriting phase.

Underwriters also flag large unexplained deposits in bank statements. When that happens, explanation letters trigger fresh reviews of the entire file, not just the flagged item. Each new submission restarts a portion of the review cycle.

Pro Tip: Gather every required document before you submit your application. Organize them into clearly labeled folders and submit complete packages the first time. One missing page costs you days, not hours.

How do appraisal and title issues affect the mortgage timeline?

Appraisal and title problems are the two most common third-party causes of delayed mortgage applications. Both involve outside parties and legal processes that borrowers cannot fully control, but they can prepare for them.

The appraisal is an independent assessment of the property's market value. Lenders require it because they will not lend more than the home is worth. When the appraised value falls below the purchase price, the loan approval stalls. You then face three options:

Renegotiate the purchase price with the seller

Cover the gap with a larger down payment

Challenge the appraisal by requesting a second opinion with supporting comparable sales data

Each of these paths takes time. Renegotiation requires seller agreement. A second appraisal requires scheduling, payment, and a new review period. Even the simplest resolution adds days to your closing timeline.

Title issues are less visible but equally disruptive. A title search examines the full ownership history of a property to confirm the seller has the legal right to sell it. Title problems such as liens or zoning issues can add 3–5 days or more to closing. In more serious cases involving probate disputes or boundary conflicts, resolution requires legal processes that can extend timelines by weeks.

Common title complications include:

Unpaid property tax liens from a prior owner

Mechanic's liens from contractors who were never paid

Boundary or easement disputes with neighboring properties

Probate issues when a previous owner died without a clear will

Pro Tip: Ask your real estate attorney or title company to begin the title search as early as possible. Early discovery of a lien gives you time to resolve it before it becomes a closing emergency.

In what ways does income verification contribute to mortgage delays?

Income verification is the process lenders use to confirm that your earnings are stable, consistent, and sufficient to support the loan. It is one of the most detailed parts of underwriting, and changes to your financial situation during processing can extend the timeline significantly.

Lenders look for a two-year history of stable income. W-2 employees can usually satisfy this with pay stubs and tax returns. The complications arise when income comes from multiple sources, includes bonuses or commissions, or comes from self-employment. Self-employed borrowers face longer delays because lenders must analyze business tax returns, profit and loss statements, and sometimes business bank accounts alongside personal financials.

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. Most lenders prefer a DTI below 43–50%. Denial rates increase by 15–17 percentage points when DTI crosses 50%. That number shows how quickly a new car loan or credit card balance opened during processing can push your application into a higher-risk category.

Financial changes during the approval process are a major source of avoidable delays. Actions that trigger re-verification include:

Opening new credit accounts or taking on new debt

Making large cash purchases outside of normal spending patterns

Changing jobs or switching from salaried to contract employment

Depositing large sums without a clear paper trail

Any of these changes can require the underwriter to restart income and asset verification from the beginning.

Pro Tip: Treat the period between application and closing as a financial freeze. Do not open new credit, change jobs, or make large purchases until after you have the keys.

What lender-side factors slow down mortgage approval speed?

Lender-side delays are real and more common than most borrowers expect. High application volume, staffing shortages, and seasonal demand spikes all create processing bottlenecks that have nothing to do with your file.

Lender backlogs during peak periods extend mortgage processing times well beyond normal estimates. Spring and early summer are historically the busiest seasons for home purchases. When application volume surges, underwriters carry heavier caseloads and review times stretch. This is a systemic issue, not a reflection of your application's quality.

Automated underwriting systems like Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor can process straightforward applications quickly. Manual underwriting, required for complex income situations or non-conforming loans, takes significantly longer because a human underwriter must review every detail of the file.

Conditional approvals add another layer of delay that borrowers often do not anticipate. Underwriters issue conditional approvals listing specific conditions the borrower must fulfill before final approval. Each document submitted in response triggers a new full review of the file. One slow document response from a borrower can stall the entire approval chain.

Borrower responsiveness directly affects timeline speed. When a lender sends a condition request and the borrower takes three days to respond, that delay multiplies across every subsequent step. Lenders also sometimes experience internal issues unrelated to your file. Software upgrades or internal audits at the lender's office can slow processing without any warning to the borrower.

Pro Tip: Check your email and phone daily during underwriting. Respond to every condition request the same day you receive it. One fast response can save you a week.

Key Takeaways

Mortgage approval delays are predictable and largely preventable when borrowers understand the specific causes and respond to lender requests without delay.

Point | Details |

|---|---|

Documentation is the top delay cause | Submit complete, legible, and current documents the first time to avoid resubmission cycles. |

Appraisal gaps stall closings | A low appraisal requires renegotiation or a larger down payment, both of which add days to closing. |

Title issues need early attention | Title problems like liens can add 3–5 days or more; start the title search as early as possible. |

Financial changes restart verification | New debt or job changes during processing can force underwriters to re-verify income from scratch. |

Borrower response speed matters | Slow replies to condition requests multiply delays across the entire approval chain. |

What I've learned about mortgage delays after years in the field

Most borrowers arrive at underwriting believing the hard part is over. Pre-approval feels like a finish line. It is not. Pre-approval is a preliminary assessment based on self-reported information. Real verification happens at underwriting, and that is where new issues surface that no one anticipated at the application stage.

The borrowers who close fastest are not the ones with perfect credit scores. They are the ones who treat document requests as urgent, keep their finances completely stable during processing, and communicate proactively with their loan officer. I have seen strong applications stall for two weeks because a borrower waited to gather one bank statement.

The other thing I tell every client is this: if your loan officer goes quiet, ask direct questions. Lenders sometimes experience internal delays from audits or system issues that have nothing to do with your file. You have the right to know where your application stands. Staying informed is not being difficult. It is being a prepared borrower.

Delays and denials are often procedural, not permanent. Receiving detailed denial reasons gives you a clear path to fix the issue, whether that means paying down debt, resolving a credit dispute, or waiting for a title lien to clear. Understanding the process does not just reduce anxiety. It gives you real control over the outcome.

— David Mordue

How David Mordue - Forward Financial Group helps you close faster

Knowing why mortgage approval delays happen is the first step. Having an experienced broker in your corner is what turns that knowledge into a faster closing.

David Mordue - Forward Financial Group offers a fully online mortgage application process designed to move quickly. The goal is funding in less than 21 days, which requires getting documentation right from the start. Whether you are a first-time buyer working through FHA loan requirements or a homeowner exploring refinancing options, the team at David Mordue - Forward Financial Group provides personalized guidance at every stage. Use the mortgage pre-approval service to start with a clear picture of your financial position before you make an offer. A strong pre-approval, backed by complete documentation, is the most effective way to reduce delays before they start.

FAQ

How long does mortgage approval typically take?

The full mortgage process from application to closing typically takes 42–50 days. Pre-approval alone usually takes 1–3 days when documentation is complete.

What is the most common reason a mortgage gets delayed?

Incomplete or missing documentation is the most frequent cause of delayed mortgage applications. A single missing document can pause the underwriting review and restart the clock on that portion of the file.

Can a low appraisal kill a mortgage approval?

A low appraisal does not automatically end the process, but it does require action. You must renegotiate the purchase price, increase your down payment, or challenge the appraisal with a second opinion, all of which add time to closing.

Does changing jobs during the mortgage process cause delays?

Yes. Changing jobs during processing triggers income re-verification. Switching from salaried to self-employed employment is especially disruptive and can require a full restart of the income review.

What is a conditional approval in mortgage underwriting?

A conditional approval means the underwriter has reviewed your file but requires additional documents or clarifications before issuing final approval. Each condition you fulfill triggers a new review, so responding quickly to every request is critical.