A refinance appraisal is a licensed appraiser's formal estimate of your home's current market value, required by your lender before approving a new loan. The appraisal process for refinancing protects the lender by confirming the property is worth at least as much as the loan amount. Without it, no lender can responsibly set your loan terms. Understanding how this process works gives you real control over your refinancing outcome, from the rate you receive to whether your application is approved at all.

What happens during the appraisal process for refinancing?

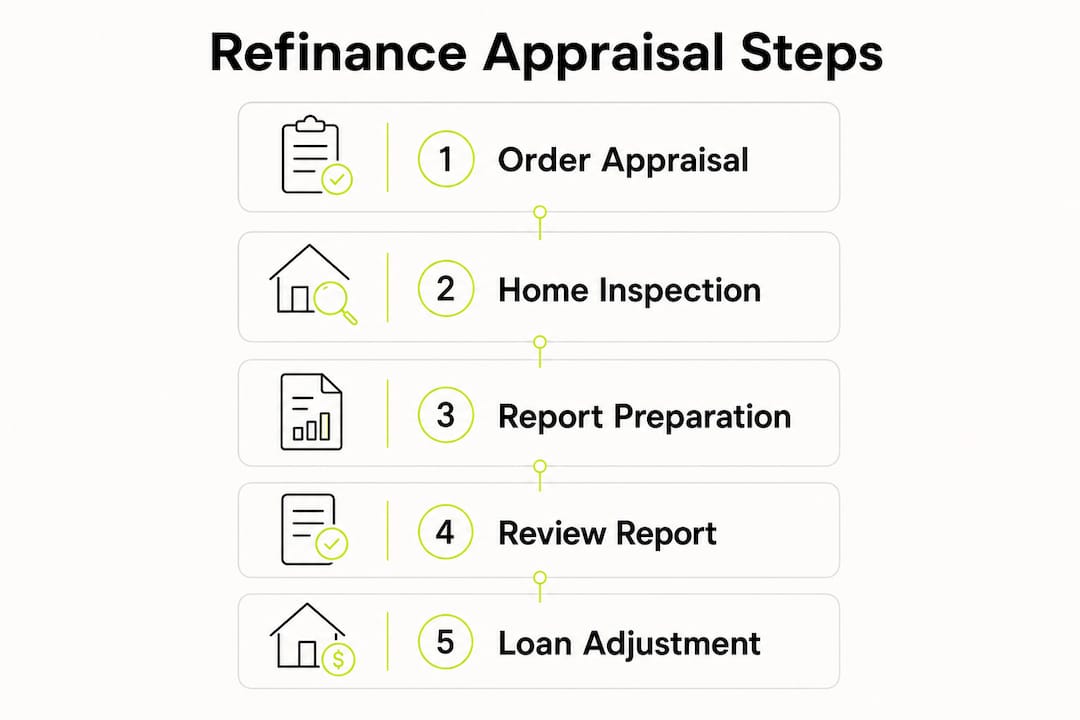

The appraisal process follows a clear sequence. Knowing each step helps you avoid surprises and stay on schedule.

Lender orders the appraisal. After you submit your refinance application, your lender selects a licensed appraiser. You typically pay the appraisal fee upfront, before the visit occurs.

Appraiser schedules the on-site inspection. The on-site inspection lasts 30–60 minutes. The appraiser walks through your home, measures square footage, notes condition, and photographs key areas.

Appraiser analyzes comparable sales. After the visit, the appraiser reviews recent sales of similar homes nearby, called "comps." These sales anchor the final value estimate.

Appraisal report is delivered to the lender. The full appraisal process typically takes 7–21 days from order to delivery. Your lender reviews the report before issuing a loan decision.

You receive a copy. Federal law requires lenders to give you a copy of the appraisal at least three business days before closing.

Loan type affects what the appraiser looks for. Conventional loans focus primarily on market value. FHA and VA loans require the appraiser to also verify Minimum Property Requirements, covering safety items like roof condition, peeling paint, and working mechanical systems. If your home fails those checks, repairs may be required before the loan closes.

Pro Tip: Ask your lender which appraisal form applies to your loan type before the inspection. Knowing the standard in advance lets you address any likely deficiencies ahead of time.

How to prepare your home for a refinancing appraisal

Preparation directly affects your appraisal result. Appraisers work from what they can see and document, so presenting your home well is both practical and financially worthwhile.

Clean and declutter every room. A clean home signals good maintenance. Clutter can obscure condition issues and make rooms appear smaller.

Improve curb appeal. Mow the lawn, trim hedges, and touch up peeling exterior paint. First impressions shape the appraiser's overall perception before they step inside.

Create a one-page list of upgrades. Documented improvements with costs and dates give the appraiser concrete evidence to credit in the report. Include new HVAC systems, roof replacements, kitchen renovations, and added square footage.

Provide full access to all areas. Appraisers cannot value inaccessible spaces. A locked attic or blocked crawl space gets estimated at average or below-average condition, which pulls your value down.

Fix minor visible defects. Broken fixtures, cracked tiles, and damaged drywall are easy to repair and signal deferred maintenance to an appraiser.

Gather permits for major work. Unpermitted additions can actually reduce value. Having permits on hand proves the work was done legally and to code.

Pro Tip: Be present during the appraisal visit. You can answer questions, point out recent upgrades, and hand the appraiser your improvement summary directly. You cannot influence the appraiser's opinion, but you can make sure they have complete information.

What do appraisals cost and how long do they take?

Appraisal costs and timelines vary by property type, location, and loan program. Planning around these variables protects your rate lock and your closing date.

Appraisal type | Typical fee | Typical timeline |

|---|---|---|

Standard single-family (conventional) | 7–21 days | |

Large or high-cost market property | $700–$1,500 | 14–28 days |

VA loan appraisal | 10–21 days | |

VA reinspection (post-repair) | $150 additional | 5–10 days |

Appraisal waiver (eligible borrowers) | $0 | 0 days |

The appraisal phase causes the longest delays in the refinancing timeline, with turnaround ranging from 7 to 28 days depending on appraiser availability and market demand. That range matters when your rate lock has an expiration date.

Appraisal waivers are worth checking before you order a full appraisal. In 2026, eligible borrowers can skip the physical appraisal entirely, saving $500–$700 and cutting 7–14 days from their closing timeline. Fannie Mae's Desktop Underwriter and Freddie Mac's Loan Product Advisor both offer waiver eligibility checks. Your lender runs these automatically during underwriting, but you can ask about eligibility upfront.

VA appraisals carry specific fee caps set by the Department of Veterans Affairs, and a $150 reinspection fee applies when a property requires repairs before final approval. If you are refinancing with a VA loan, budget for this possibility if your home has deferred maintenance.

How does appraisal value affect your refinancing options?

The appraised value determines your loan-to-value ratio, abbreviated as LTV. LTV is calculated by dividing your loan amount by the appraised value. That single number shapes your interest rate, your PMI status, and whether your loan is approved at all.

A high appraisal improves your LTV, which reduces lender risk. Lower LTV can eliminate Private Mortgage Insurance, reduce your interest rate tier, or qualify you for loan programs with stricter value requirements. Homeowners who invested in kitchen renovations, bathroom updates, or energy-efficient upgrades often see this pay off directly in their refinance terms.

A low appraisal creates the opposite problem. If the appraised value falls short of your expected loan amount, your lender may reduce the loan, require you to bring cash to closing, or deny the application. You have three options in that situation: dispute the appraisal, request a reconsideration of value with supporting comps, or accept the lower loan amount.

The reconsideration of value process is underused. You can submit comparable sales that the appraiser may have missed, particularly if your neighborhood has had recent high-value sales. Your lender submits this request on your behalf. It does not guarantee a higher value, but it is a legitimate and often effective step.

Loan type also shapes appraisal requirements in ways that affect your options:

Loan type | Appraisal focus | Key difference |

|---|---|---|

Conventional | Market value | No property condition requirements beyond basic livability |

Market value + safety | Appraiser flags health and safety defects for repair | |

VA | Market value + livability | Minimum Property Requirements; fee caps apply |

Common mistakes that delay or hurt a refinance appraisal

Most appraisal problems are preventable. The mistakes below account for the majority of delays and value shortfalls homeowners experience.

Ordering the appraisal before your loan is ready. If your application has unresolved issues, the appraisal report may expire before you close. Most appraisal reports are valid for 120 days.

Confusing appraisal with home inspection. A refinance appraisal confirms market value, not property condition. If you want a defect report, order a separate home inspection.

Blocking access to key areas. Locked attics, cluttered crawl spaces, and inaccessible mechanical rooms force the appraiser to estimate, and estimates trend conservative.

Failing to disclose improvements. If you replaced the roof two years ago but do not mention it, the appraiser may note an aging roof and reduce value accordingly.

Ignoring rate lock timing. Appraisal delays in busy markets can stretch to 3–4 weeks. If your rate lock expires during that window, you may face extension fees or a higher rate.

The fix for most of these is simple preparation and clear communication with your lender before the appraisal is ordered.

Key Takeaways

The appraisal process for refinancing determines your loan-to-value ratio, which directly controls your interest rate, PMI status, and loan approval outcome.

Point | Details |

|---|---|

Appraisal sets your LTV | Your appraised value divided by your loan amount determines your rate tier and PMI eligibility. |

Preparation changes outcomes | A one-page upgrade list and full property access can meaningfully increase your appraised value. |

Costs range widely | Standard appraisals run $350–$500; high-cost markets and VA loans can reach $1,500. |

Waivers save time and money | Eligible borrowers can skip the physical appraisal, saving $500–$700 and up to 14 days. |

Low appraisals have remedies | You can request a reconsideration of value with supporting comparable sales before accepting a reduced loan. |

What I have learned from watching homeowners navigate appraisals

Working with homeowners through the refinancing process, I have noticed one consistent pattern: the people who treat the appraisal as a passive event tend to get passive results. The homeowners who prepare, show up, and hand the appraiser a clear summary of what they have invested in the property consistently come out ahead.

The most underrated move is the one-page improvement list. I have seen it shift appraisal outcomes in real, meaningful ways. An appraiser visits dozens of homes a week. They are not going to remember that you replaced the HVAC last year unless you tell them. That document is not lobbying. It is information, and appraisers are required to consider it.

The other thing I tell every client: do not panic over a low appraisal before you have explored the reconsideration process. Appraisers are professionals, but they work from the data available to them. If recent comparable sales in your neighborhood support a higher value, that case is worth making. Most homeowners do not know this option exists, and many who use it see real results.

View the appraisal as a gatekeeper, not a verdict. You have more influence over the outcome than most people realize.

— David Mordue

Ready to move forward with your refinance?

Knowing how the appraisal process works is the first step. The next step is running the numbers to see what a refinance could actually save you.

David Mordue - Forward Financial Group offers a refinance savings calculator that lets you model different appraisal outcomes and see how your LTV affects your rate and monthly payment. If you are ready to apply, the online refinance application takes minutes to complete and can lead to funding in under 21 days. Personalized rate comparisons and expert guidance are available throughout the process, so you are never left guessing about your next step.

FAQ

What is the appraisal process for refinancing?

The appraisal process for refinancing is a licensed appraiser's formal evaluation of your home's current market value, ordered by your lender after you submit a refinance application. The result determines your loan-to-value ratio and directly affects your loan approval and interest rate.

How long does a refinance appraisal take?

The full process typically takes 7–21 days from the time the lender orders the appraisal to report delivery, with the on-site inspection itself lasting 30–60 minutes. In high-demand markets, turnaround can extend to 28 days.

Can I skip the appraisal when refinancing?

Eligible borrowers may qualify for an appraisal waiver through Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor, saving $500–$700 and cutting up to 14 days from the closing timeline. Ask your lender to check your eligibility before ordering a full appraisal.

What happens if my home appraises for less than expected?

A low appraisal reduces your available loan amount and may require you to bring cash to closing or accept a higher rate. You can request a reconsideration of value by submitting comparable sales your appraiser may have missed.

Do FHA and VA refinances have different appraisal requirements?

Yes. FHA and VA appraisals include Minimum Property Requirements that cover safety and livability items such as roof condition, peeling paint, and functioning mechanical systems. Conventional appraisals focus solely on market value without these additional property checks.