A streamlined refinance process is a reduced-documentation mortgage refinance designed exclusively for existing FHA, VA, or USDA loan holders to lower their interest rates or monthly payments with less paperwork and faster closing times. The industry term for this approach is "streamline refinance," and it refers to a specific category of government-backed refinance programs that waive or minimize requirements for appraisals, income verification, and credit checks. These programs exist because HUD, the VA, and the USDA each recognize that borrowers with proven payment histories pose lower risk, making full underwriting unnecessary. If you already hold a government-backed mortgage and want to reduce your costs quickly, this guide covers everything you need to know.

What is a streamlined refinance process and who qualifies?

Streamlined refinance programsare simplified, government-backed mortgage options that reduce paperwork and underwriting for existing FHA, VA, or USDA loan holders. The core idea is straightforward: because you already qualified for the original loan and have been making payments, lenders and government agencies accept a lower level of documentation to approve the new loan. This makes the process faster and less expensive than a traditional refinance.

Core eligibility requirements

Qualifying for a streamline refinance requires meeting several specific conditions. These apply across FHA, VA (called the Interest Rate Reduction Refinance Loan, or IRRRL), and USDA programs, though exact rules vary by loan type.

Existing government-backed loan. Your current mortgage must be an FHA, VA, or USDA loan. Conventional loans do not qualify for these programs.

Current payment status. Your existing mortgage must be current, with no recent delinquencies. Most programs require 3–6 months of on-time payments before you can apply.

210-day seasoning period. You must have closed your original loan at least 210 days before applying for the streamline refinance. This prevents serial refinancing that doesn't benefit the borrower.

Net tangible benefit. The refinance must deliver a measurable financial improvement. The net tangible benefit rule requires lenders to confirm your new loan lowers your monthly payment by at least $50, reduces your interest rate, or moves you from an adjustable rate to a fixed rate.

No cash-out. Most streamline programs only allow rate-and-term refinancing. You cannot pull equity out of your home through this type of loan.

Payment history. Lenders typically look for a clean 12-month payment record, though the minimum is 6 months of on-time payments.

Borrowers with conventional loans should be cautious about lender marketing that promises a "streamlined" refinance. These programs apply to government-backed loans only, and any similar-sounding offer for a conventional mortgage is a different product with different rules.

How does the streamline refinance process compare to a traditional refinance?

The biggest difference between a streamline refinance and a traditional refinance is what lenders skip. A traditional refinance requires a full appraisal, complete income verification, employment confirmation, and a thorough credit review. A streamline refinance eliminates or reduces most of those steps.

Streamlined refinances do not require an appraisal in most cases. This matters most for borrowers who owe close to or more than their home's current market value, since a low appraisal can kill a traditional refinance. Skipping the appraisal also saves a few hundred dollars in upfront costs and removes a common source of delay.

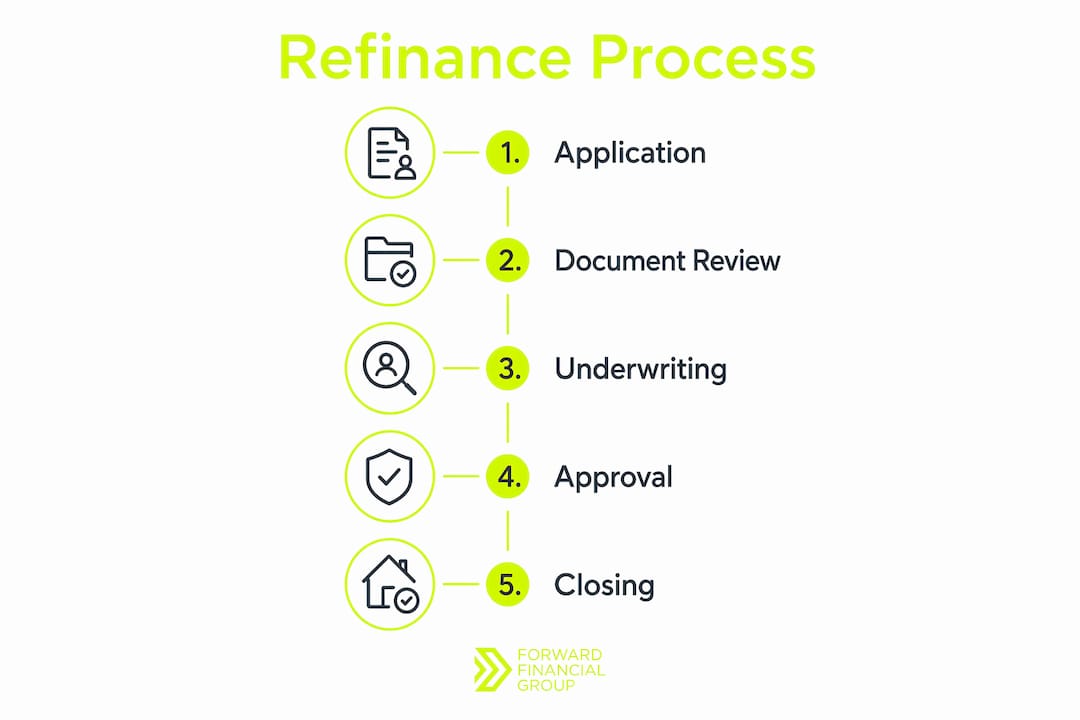

Step-by-step: how the process works

Confirm eligibility. Verify your current loan type, check your payment history, and confirm you've passed the 210-day seasoning period.

Contact your lender or shop for a new one. You are not required to stay with your current lender. Shopping multiple offers gives you better rate options.

Submit your application. Documentation requirements are minimal. You'll typically provide your current loan information and recent mortgage statements.

Lender review. The lender confirms net tangible benefit, checks your payment history, and may run a credit check depending on the program and lender.

Closing. Once approved, you sign the new loan documents. The old loan is paid off, and the new loan takes effect.

Typical closing time for streamline refinances ranges from 20 to 30 days, compared to 30–45 days for a conventional refinance. That faster timeline is a real advantage when interest rates are moving and you want to lock in a lower rate quickly.

Pro Tip: Responding to lender document requests within 24 hours is the single most effective way to keep your closing on schedule. Borrower responsiveness is the biggest factor in whether a streamline refinance closes in 20 days or stretches to 45.

What are the benefits and drawbacks of a streamline refinance?

A streamline refinance offers real advantages for the right borrower. It also has genuine limitations that can make it the wrong choice in certain situations. Understanding both sides helps you decide whether this path fits your goals.

Key benefits

Faster closing. The 20–30 day timeline beats traditional refinances by one to two weeks on average.

Lower upfront costs. Waiving the appraisal and reducing documentation cuts the fees you pay before closing.

No equity required. Because no appraisal is needed, underwater borrowers or those with minimal equity can still qualify.

Reduced paperwork. Less documentation means less time gathering financial records and fewer chances for a lender to find a disqualifying issue.

Credit flexibility. FHA streamlines often do not require a credit check, though some lenders may still request one. VA IRRRLs typically have minimal underwriting requirements.

Potential drawbacks

No cash-out option. If you need to access your home equity for renovations or debt consolidation, a cash-out refinance is not available through this program. You would need a different loan type.

Government loan requirement. Homeowners with conventional mortgages cannot use these programs at all.

Net tangible benefit rule. If current rates are not meaningfully lower than your existing rate, you may not qualify because the refinance cannot demonstrate sufficient savings.

Lender overlays. Individual lenders may add their own requirements on top of the government minimums, including credit score thresholds or income checks.

The net tangible benefit requirement is not just a formality. It is a legal underwriting standard that lenders must satisfy before approving the loan. If the numbers don't show clear savings, the refinance is denied regardless of your payment history.

How to prepare and apply for a streamline refinance

Preparation makes the difference between a smooth 20-day closing and a frustrating 45-day process. These steps give you the best chance of a fast, successful refinance.

Identify your current loan type. Check your mortgage statement or contact your servicer to confirm whether you have an FHA, VA, or USDA loan. This determines which program you can use.

Calculate your net tangible benefit. Use a refinance calculator to estimate your new monthly payment and compare it to your current one. If the savings are less than $50 per month, you may not meet the threshold.

Review your payment history. Pull your mortgage statements for the past 12 months. Any missed or late payments could disqualify you or require explanation.

Gather minimal documents. Even though documentation requirements are reduced, have your current loan information, recent mortgage statements, and proof of homeowners insurance ready before you apply.

Shop multiple lenders within a 45-day window. Multiple refinance inquiries within a 45-day period count as a single credit inquiry. This protects your credit score while letting you compare rates from several lenders.

Work with a lender experienced in government programs. FHA, VA, and USDA streamline refinances each have specific rules. A lender who handles these regularly will move faster and make fewer errors.

Pro Tip: If you have a VA loan, the IRRRL program is one of the most borrower-friendly refinance options available. It typically requires no appraisal, no income verification, and no out-of-pocket costs if you roll the funding fee into the loan.

Key Takeaways

A streamline refinance is the fastest, lowest-cost path to a lower rate for homeowners with existing FHA, VA, or USDA loans, provided the net tangible benefit requirement is met.

Point | Details |

|---|---|

Government loans only | Streamline refinances apply exclusively to FHA, VA, and USDA mortgages, not conventional loans. |

210-day seasoning rule | Your original loan must be at least 210 days old before you can apply for a streamline refinance. |

Net tangible benefit required | The refinance must lower your payment by at least $50 or improve your loan terms to be approved. |

Faster closing timeline | Streamline refinances close in 20–30 days, compared to 30–45 days for a traditional refinance. |

Shop within 45 days | Comparing multiple lenders within a 45-day window counts as one credit inquiry and protects your score. |

What I've learned about streamline refinances after years in the field

Most homeowners assume a streamline refinance is a guaranteed approval because the documentation requirements are lighter. That assumption costs people time and creates real frustration when a denial comes through.

The net tangible benefit rule is where most applications run into trouble. If rates have not dropped enough since your original loan closed, the math simply doesn't work. I've seen borrowers with perfect payment histories get denied because their rate reduction was too small to meet the threshold. The rule exists to protect you from refinancing into a loan that doesn't actually save you money, but it also means timing matters as much as eligibility.

The other factor most borrowers underestimate is their own role in the timeline. Lenders can move quickly on streamline refinances because the underwriting is lighter. The delays almost always come from the borrower side: slow responses to document requests, missing HOA verification letters, or outdated insurance certificates. If you want to close in 20 days, treat every lender request as urgent.

One misconception worth addressing directly: some borrowers believe a streamline refinance is a way to access home equity quickly. It is not. The no-cash-out rule is firm across FHA and USDA programs, with very limited exceptions on the VA side. If equity access is your goal, a different loan product is the right tool.

My recommendation is to consult a mortgage professional who works with government-backed loans regularly before you apply. The eligibility rules are specific, and a lender who handles FHA streamlines and VA IRRRLs daily will give you a realistic picture of your options and timeline.

— David Mordue

Ready to see if a streamline refinance makes sense for you?

If you hold an FHA, VA, or USDA mortgage and rates have moved since you closed, the numbers may work in your favor right now. David Mordue - Forward Financial Group offers a fully online application process with funding possible in less than 21 days, which aligns directly with the speed advantage a streamline refinance provides.

Use the refinance savings calculator to estimate your new monthly payment and see whether you meet the net tangible benefit threshold before you apply. When you're ready to move forward, start your refinance application with David Mordue - Forward Financial Group for personalized rate comparisons and expert guidance through every step of the process.

FAQ

What is a streamlined mortgage refinance?

A streamlined mortgage refinance is a government-backed program that lets existing FHA, VA, or USDA loan holders refinance with reduced documentation, no appraisal in most cases, and faster closing times than a traditional refinance.

How quickly can a streamline refinance close?

Streamline refinances typically close in 20–30 days, compared to 30–45 days for a conventional refinance. Borrower responsiveness to lender requests is the primary factor in reaching the faster end of that range.

Can I get cash out with a streamline refinance?

No. Streamline refinance programs are limited to rate-and-term refinancing. Cash-out refinancing is not permitted under FHA or USDA streamline programs, with only narrow exceptions available under the VA IRRRL.

Do I need a new appraisal for a streamline refinance?

Most streamline refinance programs waive the appraisal requirement entirely. This benefits borrowers with low or no equity, since a low appraisal cannot block the refinance.

How many on-time payments do I need to qualify?

Most programs require a minimum of 6 months of on-time payments and a 180-day seasoning period from your original loan closing date before you can apply for a streamline refinance.