The reverse mortgage application process is a federally regulated, multi-step procedure that lets homeowners age 62 or older convert home equity into tax-free income without selling their home. The formal term is a Home Equity Conversion Mortgage, or HECM, which is the FHA-insured version that most borrowers use. Understanding each step before you begin saves time, prevents costly delays, and protects your financial security in retirement. The full process typically runs 30–45 days from counseling through funding, with mandatory HUD counseling and a home appraisal as the two most time-sensitive steps.

What are the reverse mortgage application process steps?

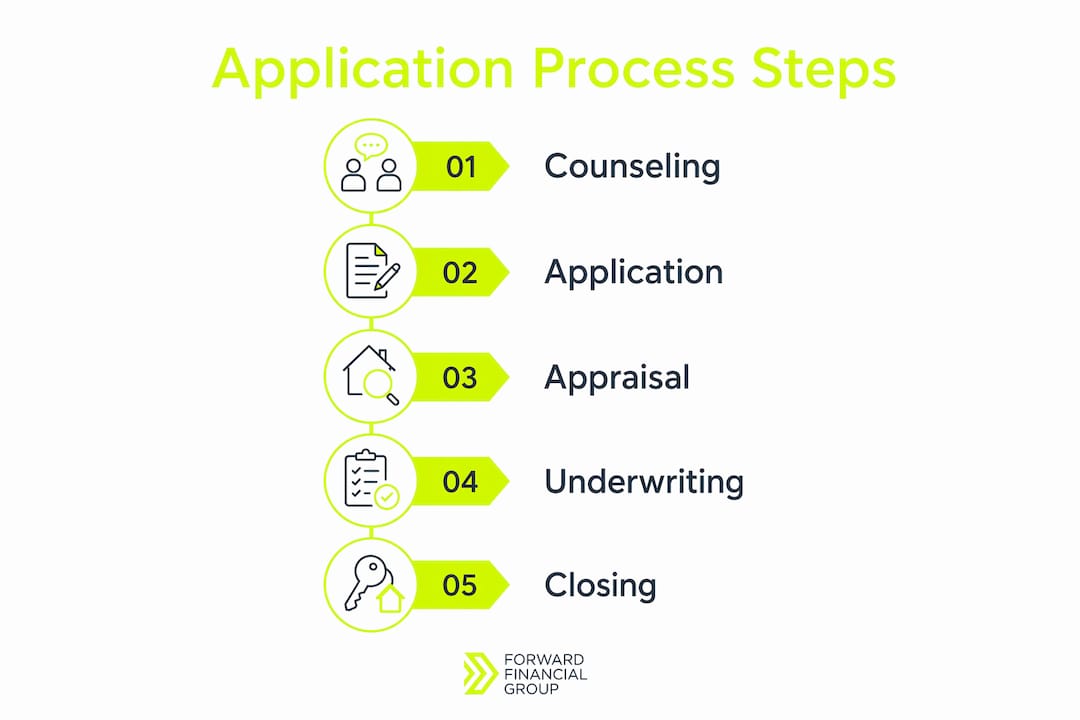

The HECM application follows a fixed sequence set by federal standards. You cannot skip or reorder the steps. The sequence is: complete HUD-approved counseling, submit your application with the counseling certificate, schedule a home appraisal, pass underwriting, close the loan, and receive your funds.

Lenders cannot order appraisals or begin underwriting until your counseling certificate is in hand. That single rule is the most misunderstood part of the process. Seniors who try to submit an application before finishing counseling cause their own delays, sometimes by weeks.

The CFPB confirms eligibility requirements: you must be 62 or older, the home must be your primary residence, and you must have sufficient equity. The loan amount depends on your age, the current interest rate, and your home's appraised value. Older borrowers with higher-value homes generally qualify for larger amounts.

What are the eligibility requirements and documents needed?

Qualifying for a HECM requires meeting three core conditions. You must be at least 62 years old. The property must be your primary residence, not a vacation home or investment property. You must have enough equity in the home, typically meaning you own it outright or carry a small remaining mortgage balance.

Gathering your documents early is the single most effective way to prevent underwriting delays. Lenders require a specific set of paperwork before they can process your file.

Required documents include:

Government-issued photo ID and proof of age (passport or birth certificate)

Property deed showing ownership

Recent mortgage statements if a balance remains

Proof of income: Social Security award letters, pension statements, or retirement account statements

Homeowners insurance declarations page

Recent property tax statements

Flood insurance documentation if applicable

Pro Tip: Organize all documents into a single folder, physical or digital, before your counseling appointment. Lenders who receive complete files at submission move to appraisal faster.

The table below shows which documents are used at each stage of the process.

Document | Used at Stage |

|---|---|

Photo ID and birth certificate | Application submission |

Property deed | Application and underwriting |

Mortgage statements | Underwriting |

Income proof (Social Security, pension) | Underwriting |

Homeowners insurance declarations | Underwriting and closing |

Property tax statements | Underwriting |

Standard documentation requirements from lenders consistently include all items above. Missing even one document can pause underwriting and add days to your timeline.

Why is reverse mortgage counseling required?

Counseling is a federally mandated consumer protection, not an optional orientation. HUD requires counseling with an approved agency before any lender can process your HECM application. The certificate you receive at the end is a legal prerequisite for moving forward.

The counseling session covers everything you need to make an informed decision. Topics include how the loan works, total costs, your long-term obligations, and alternatives such as refinancing or downsizing. You also discuss what happens when you move out, sell, or pass away.

A complete reverse mortgage counseling checklist covers:

How loan balances grow over time

Upfront and ongoing costs, including mortgage insurance premiums

Your obligation to pay property taxes, homeowners insurance, and maintain the home

Payout options: lump sum, line of credit, monthly payments, or a combination

Alternatives to a reverse mortgage

Spousal protections if one borrower is under 62

Counseling is designed to ensure you fully understand your obligations before you sign anything. Treat it as a paid financial education session, not a bureaucratic hurdle.

Preparing household budget details before your session, including monthly expenses, property charges, and any existing debts, makes the session more productive and helps the counselor assess your situation accurately. Counseling can be done by phone or in person. Fees vary by agency but are generally modest, and some agencies offer free sessions for low-income borrowers.

Pro Tip: Write down your questions before the counseling call. Counselors are required to answer them fully, and a prepared borrower gets far more value from the session.

What happens from application submission to loan funding?

Once you hold your counseling certificate, the active application phase begins. Each step below builds on the previous one, and the overall timeline runs approximately 30–45 days.

Submit your application. Attach your counseling certificate and all required documents. Your lender reviews the file for completeness before ordering the appraisal.

Home appraisal. A HUD-approved appraiser visits your property to determine its current market value and condition. The appraisal drives your loan amount. If the appraiser notes required repairs, those must be addressed before closing.

Underwriting. The lender verifies every document, confirms your income, checks property taxes and insurance status, and assesses your ability to meet ongoing obligations. Underwriters may request additional documents during this phase.

Conditional approval. The lender issues approval with any remaining conditions, such as updated insurance documents or a repair completion certificate.

Closing. You sign final loan documents, often at your home or a title company. Federal law gives you a three-business-day right of rescission after signing. You can cancel without penalty during that window.

Fund disbursement. After rescission ends, funds are released. Cash disbursement can take several weeks from the start of the process, so plan your retirement income timing accordingly.

The table below shows the typical time each phase takes.

Phase | Estimated Duration |

|---|---|

Counseling | 1–3 days to schedule and complete |

Application submission | 1–2 days |

Appraisal scheduling and completion | 1–2 weeks |

Underwriting | 1–2 weeks |

Closing and rescission | 4–5 business days |

Fund disbursement | 1–3 business days after rescission |

You can choose how to receive your funds. Options include a lump sum, a line of credit you draw from as needed, fixed monthly payments for a set term, or a combination. Each option has different cost and tax implications, which your counselor will explain.

What are common mistakes to avoid during the application?

Most delays in the HECM process are preventable. Appraisal scheduling and underwriting review are the two most common bottlenecks, and both respond well to preparation.

Mistakes that slow or derail applications:

Submitting the application before completing counseling, which forces the lender to wait

Providing incomplete documents at submission, triggering underwriting back-and-forth

Deferring home maintenance, which can cause appraisal conditions that delay closing

Underestimating ongoing obligations for property taxes, insurance, and upkeep

The obligation point deserves emphasis. The loan balance grows over time, and failing to stay current on property taxes or homeowners insurance can trigger early repayment or default. This is not a theoretical risk. It is the most common reason borrowers lose their homes after taking a reverse mortgage.

The application process is not just paperwork. It is an affordability screening. Lenders and counselors are assessing whether you can sustain the home financially for the long term.

Pro Tip: Before applying, run a 12-month budget that includes property taxes, insurance premiums, and estimated maintenance costs. If those numbers are tight, discuss alternatives with your counselor before proceeding.

Clear communication with your lender speeds up every phase. Respond to document requests within 24–48 hours. Ask your loan officer for a checklist of outstanding items after submission so nothing falls through the cracks.

Key Takeaways

The reverse mortgage application process requires counseling, documentation, appraisal, underwriting, and closing in a fixed federal sequence that typically takes 30–45 days from start to funding.

Point | Details |

|---|---|

Counseling comes first | HUD-approved counseling and a certificate are required before any lender can process your application. |

Documents determine speed | Submitting a complete file at application prevents underwriting delays and keeps the timeline on track. |

Appraisal drives loan amount | Your home's appraised value and condition directly affect how much you can borrow and whether repairs are required. |

Ongoing obligations are non-negotiable | Staying current on property taxes, insurance, and maintenance is required to avoid default after closing. |

Plan for the full timeline | Expect 30–45 days from counseling to funding and plan your retirement income needs around that window. |

What I've learned after years of helping seniors with this process

Most seniors I work with come in thinking the reverse mortgage application is primarily about paperwork. It is not. The counseling session is the most important hour in the entire process. Borrowers who treat it seriously, who show up prepared with their budget and their questions, consistently have smoother applications and fewer surprises at closing.

The other thing I see repeatedly: people rush. They want to skip counseling or submit before they have all their documents because they need funds quickly. That urgency almost always backfires. A missing insurance document or an unscheduled appraisal adds two weeks, not two days. Patience in the early stages pays off at closing.

One more thing that rarely gets said plainly: a reverse mortgage is a long-term commitment. The loan balance grows every month. If you cannot reliably cover property taxes and insurance on your current income, a reverse mortgage may not be the right tool. Your counselor will tell you this, and I will tell you this too. The goal is financial security, not a short-term fix that creates a larger problem later. Working with a trusted advisor who will give you that honest assessment is worth more than any rate comparison. You can use a refinance calculator to model how your current mortgage costs compare before making any final decisions.

— David Mordue

Guidance from David Mordue - Forward Financial Group

Navigating the HECM process is straightforward when you have the right support from the start. David Mordue - Forward Financial Group works with seniors to assess eligibility, organize documentation, and coordinate every phase from counseling through closing.

Whether you are evaluating a reverse mortgage for the first time or ready to move forward with an application, the team at David Mordue - Forward Financial Group provides personalized guidance at every step. Visit davidmordue.com to request a consultation, review current mortgage rate options, or use the FHA loan resources to understand how FHA-insured products fit your retirement plan. Getting the right information early makes the entire process faster and less stressful.

FAQ

What is the minimum age to apply for a reverse mortgage?

You must be at least 62 years old to qualify for a HECM reverse mortgage. If you have a spouse under 62, specific non-borrowing spouse protections apply and should be discussed during counseling.

How long does the reverse mortgage application process take?

The process typically takes 30–45 days from counseling completion through fund disbursement. Appraisal scheduling and underwriting are the phases most likely to extend that timeline.

Can I apply for a reverse mortgage before completing counseling?

No. Counseling must be completed and the certificate received before a lender can accept or process your application. Submitting early does not speed things up.

What documents do I need to apply for a reverse mortgage?

You need a government-issued photo ID, proof of age, property deed, mortgage statements, income documentation such as Social Security award letters, and your homeowners insurance declarations page.

What happens if I miss a property tax or insurance payment after closing?

Missing property tax or insurance payments can trigger a default on your reverse mortgage. The CFPB notes that staying current on property charges is a core borrower obligation and failure to do so can result in early loan repayment requirements.