A pre-approved buyer advantage is defined as the competitive edge a homebuyer gains when a lender issues a conditional mortgage commitment based on verified financial information, not just self-reported estimates. Sellers and real estate agents treat this letter as proof that you are a serious, qualified buyer. The standard industry term for this status is mortgage pre-approval, and it carries far more weight than the informal pre-qualification many buyers mistake for the same thing. Whether you are purchasing your first home or adding to an investment portfolio, understanding this distinction can determine whether your offer wins or loses in a competitive market.

What is a pre-approved buyer advantage in mortgage financing?

A pre-approved buyer advantage means a lender has reviewed your actual financial documents and issued a conditional commitment to lend up to a specific amount. This is not a guarantee of final loan approval, but it is a strong signal that you meet the lender's requirements based on real data. Freddie Mac describes pre-approval as an indication of lending willingness, with final approval still depending on the property appraisal and last-stage verifications.

The core value of this status is credibility. When you submit an offer with a pre-approval letter attached, sellers see that a lender has already done the work of checking your income, assets, and credit. That reduces their perceived risk and makes your offer feel safer than one from a buyer who has only been pre-qualified. In competitive markets, that difference often determines which offer gets accepted.

Pre-approval also gives you a clear budget ceiling. You know exactly how much a lender is willing to extend, which prevents you from wasting time on homes outside your range. For real estate investors, this clarity is especially useful when evaluating multiple properties simultaneously.

How does mortgage pre-approval work and what documentation is required?

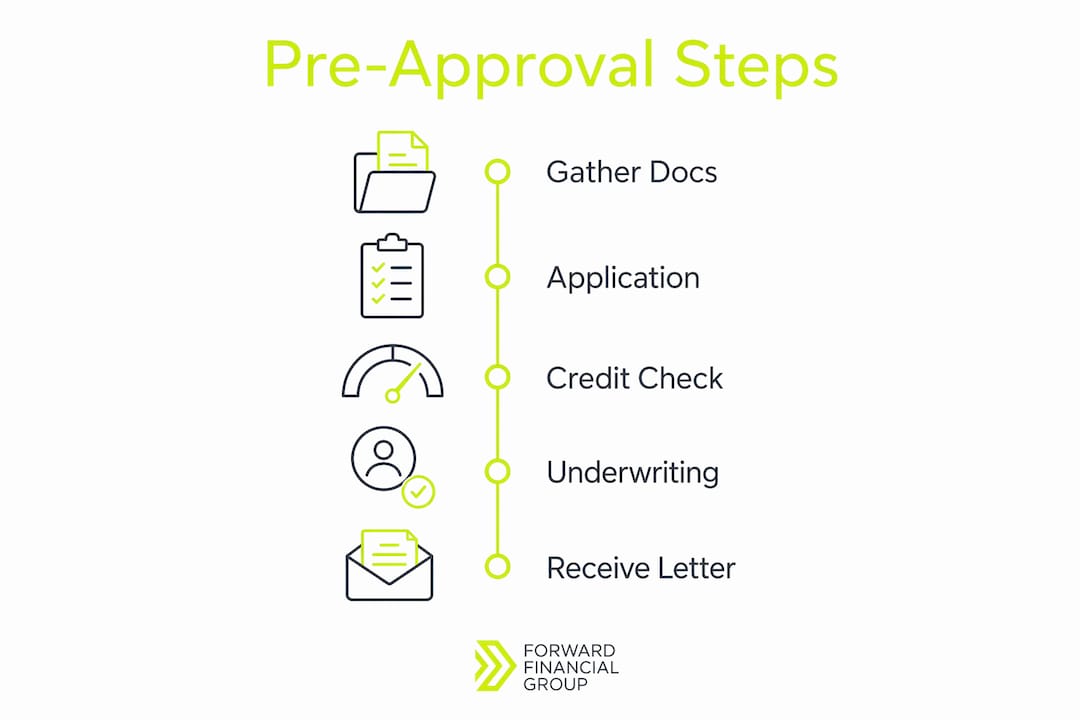

The pre-approval process begins when you formally apply with a lender and submit a complete package of financial documents. Lenders evaluate your application using what the industry calls the four C's: capacity (your income and debt load), capital (your assets and savings), collateral (the property itself), and credit (your credit history and score). Each factor influences both your approval status and the loan terms you receive.

Lenders typically require the following documents to issue a pre-approval letter:

W-2 forms from the past two years to verify employment income

Recent pay stubs covering at least 30 days of earnings

Bank statements from the past two to three months showing assets and reserves

Federal tax returns from the past two years, especially for self-employed buyers

Government-issued ID and Social Security number for identity and credit verification

Once submitted, the lender pulls your credit report and runs the documents through their underwriting guidelines. This process can take anywhere from a few hours to several business days depending on the lender and the complexity of your financial picture. After review, you receive a pre-approval letter stating the loan amount, loan type, and expiration date.

Pre-approval letters expire after 30–90 days depending on the lender. That window matters. If you find a home near the end of that period, you may need to refresh your documents and get a new letter before submitting your offer.

Pro Tip: Gather all your documents before you contact a lender. A complete application package speeds up the review and reduces the chance of delays that could cost you a property in a fast-moving market.

What seller-facing benefits does pre-approval give homebuyers?

Pre-approval signals to sellers that your financing is not speculative. A seller reviewing two offers, one with a pre-approval letter and one without, will almost always favor the pre-approved buyer. The reason is straightforward: upfront underwriting allows for faster loan closing and a lower risk of the deal falling apart due to financing issues.

In multiple-offer situations, this advantage becomes decisive. Sellers and their agents know that a pre-approved buyer has already cleared the most common financing hurdles. That confidence can lead sellers to accept a slightly lower offer from a pre-approved buyer over a higher offer from an unverified one.

The buyer pre-approval advantage also affects negotiation dynamics. When sellers trust your financing, they are more willing to negotiate on price, closing date, or contingencies. That flexibility can translate into real savings or better terms.

Pre-qualification vs. pre-approval: what sellers actually see

Factor | Pre-qualification | Pre-approval |

|---|---|---|

Financial verification | Self-reported only | Documented and lender-verified |

Credit check | Usually not required | Hard credit pull required |

Underwriting review | None | Completed before letter issuance |

Seller confidence level | Low | High |

Negotiation strength | Weak | Strong |

Typical validity | Informal, no set expiration | 30–90 days from issuance |

The table above shows why sellers respond more strongly to verified pre-approval. Pre-qualification is simply a lender's rough estimate based on what you tell them. Pre-approval is a documented finding based on what you can prove.

Key seller-facing benefits of pre-approval include:

Reduced risk of financing contingency failures

Faster path to closing because underwriting is largely complete

Greater confidence in the buyer's ability to perform

Stronger negotiating position on price and terms

How does pre-approval differ from pre-qualification, and why does it matter?

Pre-qualification is an informal estimate. A lender asks about your income, debts, and assets, and gives you a rough loan range based on what you report. No documents are verified. No credit report is pulled. The result is a number that tells you very little about what you will actually qualify for.

Pre-approval is the opposite. Documented verification is required, a hard credit inquiry is conducted, and the lender's underwriting team reviews your full financial picture before issuing a letter. That letter carries real weight because it reflects actual findings, not estimates.

Many buyers make the mistake of treating pre-qualification as sufficient before they start shopping. This creates two problems. First, you may be shopping in the wrong price range. Second, when you find a home and submit an offer, sellers and agents will recognize immediately that your financing has not been verified. That weakens your position before negotiations even begin.

Common pitfalls of relying on pre-qualification:

Overestimating your actual buying power

Losing offers to pre-approved buyers in competitive markets

Discovering disqualifying issues late in the process, after you are emotionally invested in a property

Wasting time on homes outside your verified budget

Pro Tip: Get pre-approved before you start touring homes. Knowing your verified limit shapes your search and prevents the frustration of falling in love with a property you cannot finance.

How can buyers and investors use the pre-approved buyer advantage effectively?

Holding a pre-approval letter is only part of the advantage. How and when you use it determines whether it actually strengthens your offer. Timing the letter's validity with your offer submission is critical. A letter that expires before closing adds friction and may require you to restart the process.

Follow these steps to get the most from your pre-approval status:

Keep your finances stable. Avoid new credit applications, large purchases, or job changes between pre-approval and closing. Any material change can trigger re-verification and potentially void your approval.

Align your letter with your offer timeline. If your pre-approval is nearing expiration, contact your lender to refresh it before submitting an offer. An expired letter signals to sellers that your financing may be uncertain.

Use the letter strategically in negotiations. Share it early in the offer process to establish credibility. In some markets, agents will not even show homes to buyers who cannot produce a pre-approval letter.

Understand the conditional nature of your approval. A conditional pre-approval means you meet general loan requirements, but final approval still depends on the property appraisal and last-stage document verification. Do not treat the letter as a guarantee.

For investors: document all income sources and reserves thoroughly. Lenders evaluating investment property loans want to see reserves and multiple income streams clearly documented. Incomplete information weakens your offer and can delay the process. Investors pursuing rental properties may also benefit from reviewing DSCR loan options, which use property income rather than personal income for qualification.

Communicate clearly with your agent and lender. Misalignment between your offer timeline and your lender's processing schedule is one of the most common reasons deals fall apart at the last stage.

The strongest buyer advantage comes not just from having the letter but from using it with precision and maintaining the financial stability that earned it in the first place.

Key Takeaways

Pre-approval is the single most effective step a homebuyer or investor can take to strengthen their position before making an offer.

Point | Details |

|---|---|

Pre-approval is verified, not estimated | Lenders review actual documents, making the letter credible to sellers and agents. |

Letters expire in 30–90 days | Time your offer submission carefully to avoid losing your verified status. |

Pre-approval beats pre-qualification | Sellers respond to documented proof, not self-reported income estimates. |

Financial stability is required | Avoid new debt or job changes between approval and closing to protect your status. |

Investors need thorough documentation | Reserves and all income sources must be fully documented for the strongest offer position. |

What I have learned about using pre-approval as a real advantage

After working with homebuyers and investors across many market conditions, the pattern I see most often is this: buyers who treat pre-approval as a formality lose deals that buyers who treat it as a tool tend to win.

The most common mistake I encounter is buyers who get pre-approved and then change their financial situation before closing. They open a new credit card, buy a car, or switch jobs. Any of those moves can trigger re-verification and delay or derail the loan. The pre-approval letter is not a finish line. It is a starting position that you have to maintain.

The second mistake is timing. I have seen buyers submit offers with letters that expire in three days. Sellers and listing agents notice. It signals that the buyer has been searching for a long time without success, which weakens their negotiating position before a single word is exchanged.

For investors, the documentation piece is where I see the most friction. Rental income, partnership distributions, and business income all require specific documentation that differs from a standard W-2 package. Getting that paperwork organized before you approach a lender saves weeks and prevents the kind of last-minute scrambles that cost you properties.

My honest advice: treat the pre-approval process as seriously as you treat the offer itself. The buyers who win in competitive markets are not always the ones with the highest bid. They are the ones whose financing is airtight, whose letters are current, and whose agents can call the listing agent and say with confidence that this deal will close.

— David Mordue

Ready to get your mortgage pre-approval?

At David Mordue - Forward Financial Group, the pre-approval process is fully online and built for speed. You can submit your application and supporting documents without visiting a branch, and funding can happen in less than 21 days. That timeline matters in competitive markets where sellers want certainty.

Whether you are a first-time buyer using an FHA loan or an investor building a portfolio, David Mordue - Forward Financial Group provides personalized rate comparisons and direct lender communication at every stage. Visit davidmordue.com to start your pre-approval application and put a verified letter in your hands before your next offer.

FAQ

What is a pre-approved buyer advantage?

A pre-approved buyer advantage is the credibility and negotiating strength a buyer gains when a lender issues a conditional mortgage commitment based on verified financial documents. Sellers treat this letter as evidence that the buyer's financing is real and reliable.

How long does a mortgage pre-approval last?

Pre-approval letters typically remain valid for 30–90 days depending on the lender. If your letter expires before you find a home, you will need to refresh your documents and request a new letter.

Is pre-approval worth it before home shopping?

Pre-approval is worth completing before you tour a single home. It confirms your verified budget, strengthens every offer you make, and prevents you from losing properties to buyers whose financing is already documented.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on self-reported information with no document verification. Pre-approval requires full documentation, a credit check, and lender underwriting review, making it far more credible to sellers.

Does pre-approval guarantee a mortgage?

Pre-approval does not guarantee final loan approval. Zillow notes that a conditional pre-approval still requires the property to appraise at value and all final verifications to be completed before the loan closes.