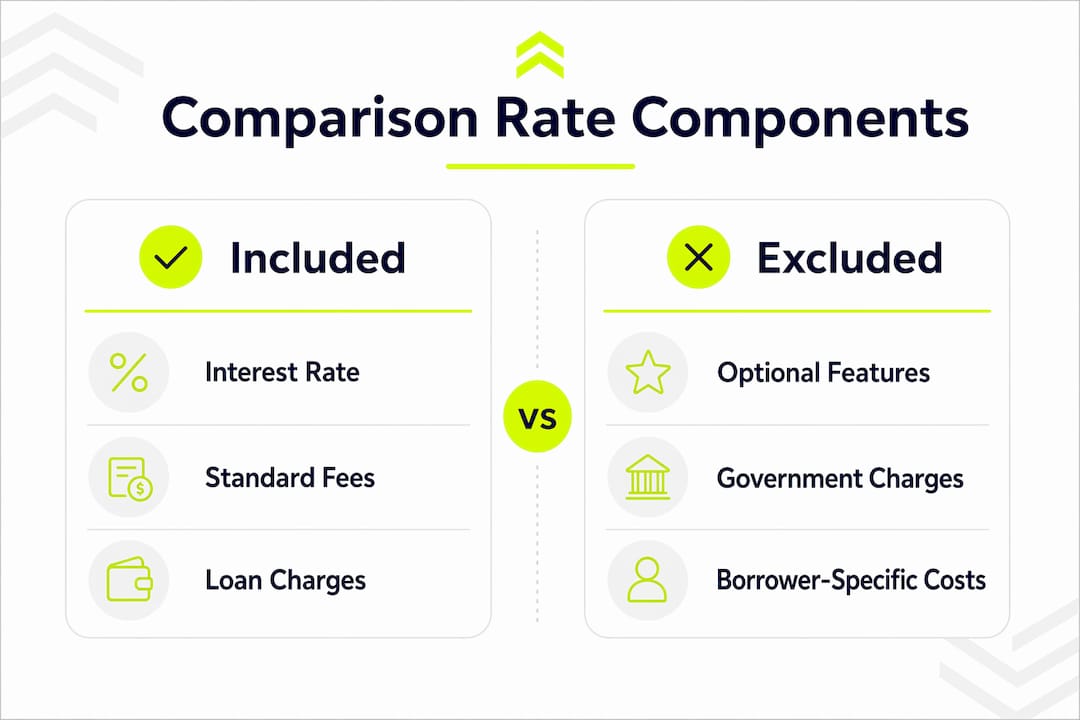

A mortgage comparison rate is a single percentage figure that combines a loan's interest rate with most of its standard fees and charges, giving you a more accurate picture of what a home loan actually costs. Most lenders advertise a low headline interest rate to attract attention, but that number alone does not reflect the full cost of borrowing. The comparison rate fills that gap. Understanding it is one of the most practical steps you can take before signing any mortgage agreement, whether you are buying your first home or refinancing an existing loan.

What is a mortgage comparison rate and how is it calculated?

A mortgage comparison rate is calculated using a standardized formula applied to a $150,000 loan over a 25-year term with monthly repayments. That formula rolls the headline interest rate together with most lender fees into one percentage. The result lets you compare loans from different lenders on equal footing.

The fees typically included in the calculation are:

Application or establishment fees paid upfront when you open the loan

Ongoing account-keeping fees charged monthly or annually

Discharge fees paid when you close or refinance the loan

Settlement fees and other standard lender charges

What the comparison rate does not include are optional features, government charges, or borrower-specific costs. That distinction matters, and we will cover it in detail below.

Here is a simple example showing how fees shift the comparison rate on two hypothetical loans:

Loan | Advertised Rate | Monthly Fee | Application Fee | Comparison Rate |

|---|---|---|---|---|

Loan A | 6.50% | $0 | $0 | 6.50% |

Loan B | 6.20% | $15 | $600 | 6.58% |

Loan C | 5.90% | $30 | $1,200 | 6.72% |

Loan C carries the lowest advertised rate but the highest comparison rate. That gap signals high fees that more than offset the rate advantage.

Pro Tip: Ask every lender for a full fee schedule before accepting a quote. The comparison rate tells you fees exist, but the schedule tells you exactly what they are.

Why is the comparison rate higher than the advertised interest rate?

The comparison rate is almost always higher than the headline rate because fees and charges add real cost to borrowing. The wider the gap between the two figures, the more you are paying in fees relative to the loan's interest cost.

A large gap between the advertised rate and the comparison rate is a direct signal that the lender charges significant fees. A gap of 0.5% or more on a standard loan warrants a close look at the fee schedule.

Common reasons for a large gap include:

High upfront application or origination fees

Recurring monthly account fees over the loan term

Discount points paid to reduce the headline rate artificially

Lender-specific charges not common across the market

Discount points deserve special attention. A lender may offer a rate of 5.75% with two discount points paid upfront, making the loan look attractive. But discount points inflate upfront costs and only make financial sense if you stay in the home long enough to recover them through lower monthly payments. If you sell or refinance within five years, you likely lose money on that trade.

Not every fee is captured in the comparison rate, either. Optional features like offset accounts, redraw facilities, and portability add value but are excluded from the standard calculation. A loan with a slightly higher comparison rate may still cost you less overall if it includes an offset account that reduces your effective interest balance.

How does the comparison rate differ from APR and interest rate?

These three figures measure different things, and confusing them leads to poor loan decisions. The table below clarifies each one:

Metric | What it measures | What it includes | Where it is used |

|---|---|---|---|

Interest rate | Cost of borrowing the principal | Principal interest only | All markets |

Comparison rate | True loan cost (standardized) | Interest rate plus standard fees | Australia primarily |

APR (Annual Percentage Rate) | True loan cost (U.S. standard) | Interest, origination fees, mortgage insurance, discount points | United States |

In the U.S., the APR is the standard equivalent of the comparison rate. The Consumer Financial Protection Bureau requires lenders to disclose APR alongside the interest rate on all loan documents. APR includes mortgage insurance premiums, origination fees, and discount points, providing a more complete view of total cost than the interest rate alone.

The key difference between APR and a comparison rate is scope. APR can include borrower-specific costs like private mortgage insurance (PMI), which varies by credit score and down payment. The comparison rate uses a fixed, standardized formula that does not adjust for individual borrower profiles. Neither metric is perfect on its own. The most reliable approach is to review both the interest rate and the APR (or comparison rate) together, then request a full Loan Estimate to see every line item.

What are the limitations of comparison rates?

The comparison rate is a guide, not a guarantee. It reflects a standardized loan scenario that may not match your actual borrowing situation. A borrower taking a $500,000 loan over 30 years will experience a different effective cost than the $150,000 over 25 years used in the standard calculation.

The most significant limitation is what the comparison rate excludes. Loan features like offset accounts are not factored into the comparison rate, even though they can reduce the interest you pay significantly over time. A loan with a 6.80% comparison rate and a full offset account may cost less in total interest than a loan with a 6.60% comparison rate and no offset.

How to compare mortgage offers effectively

Relying on comparison rates alone is not enough. The most reliable way to compare loans is to normalize every offer so you are evaluating identical conditions. Here is a step-by-step process:

Request quotes from at least three to five lenders. Borrowers who compared 3–5 lenders saved an average of $3,000, and those who obtained four quotes saved roughly $1,200 annually. More quotes give you real leverage.

Match loan terms exactly. Use the same loan amount, term length, and number of points across every quote. Comparing a 30-year loan to a 15-year loan tells you nothing useful.

Request a Loan Estimate from each lender. The Consumer Financial Protection Bureau recommends comparing at least three Loan Estimates to uncover fee variations hidden behind low headline rates. Loan Estimates list the APR, total interest percentage (TIP), and itemized fees in a standardized format.

Calculate total cost over your expected timeline. If you plan to sell in seven years, calculate total payments and fees over seven years, not the full loan term. Normalizing by timeline prevents misleading comparisons between loans with different fee structures.

Evaluate loan features separately. List features like offset accounts, redraw facilities, and extra repayment options. Assign them a value based on how you plan to use the loan.

Negotiate. Lenders expect it. Use competing Loan Estimates as leverage to request fee waivers or rate reductions.

Pro Tip: Use the Davidmordue refinance calculator to model total cost scenarios across different rate and fee combinations before you commit to any offer.

Closing costs range from 2% to 6% of the home purchase price and vary significantly between lenders. On a $400,000 home, that gap represents $8,000 to $24,000. A small difference in the advertised interest rate rarely offsets that kind of fee variation.

How understanding comparison rates saves you real money

Careful rate comparison produces measurable savings. A Freddie Mac study found that borrowers who obtained four rate quotes saved more than $1,200 annually on mortgage costs. That figure compounds significantly over a 30-year loan term.

Consider two loans on a $400,000 purchase:

Loan A: 6.50% interest rate, comparison rate 6.52%, minimal fees

Loan B: 6.20% interest rate, comparison rate 6.75%, high origination fees and monthly charges

Loan B's lower advertised rate looks attractive. But its comparison rate reveals that fees add more than 0.50% to the true cost. Over 30 years, Loan A saves tens of thousands of dollars in total interest and fees. The comparison rate caught the difference before you signed anything.

The steps that produce the most savings are straightforward:

Contact three to five lenders and request formal Loan Estimates

Compare APR figures alongside interest rates on every quote

Use a conventional affordability calculator to model how fee differences affect your monthly budget

Factor in how long you plan to keep the loan before paying discount points

Fees can outweigh interest rate differences in total loan cost, which is why the comparison rate exists as a decision-making tool in the first place. Use it as your first filter, then dig deeper with full Loan Estimates.

Key takeaways

The comparison rate is the most reliable first filter for evaluating home loan costs, but it requires supporting data to drive a sound decision.

Point | Details |

|---|---|

Comparison rate definition | It combines the interest rate and standard fees into one percentage for fair loan comparison. |

APR is the U.S. equivalent | In the U.S., APR serves the same purpose and must be disclosed on all Loan Estimates. |

Fees can exceed rate savings | Closing costs of 2%–6% of purchase price often matter more than small rate differences. |

Comparison rates have limits | They exclude offset accounts and borrower-specific costs, so always review full Loan Estimates. |

Multiple quotes save money | Borrowers who compared four lender quotes saved over $1,200 annually on average. |

My take on how borrowers actually use comparison rates

I have worked with hundreds of homebuyers and refinancing clients, and the same mistake comes up repeatedly. A borrower finds a lender advertising a rate that is 0.30% lower than everyone else, locks in mentally, and then discovers at closing that the fees add $4,000 to $6,000 to their costs. The comparison rate would have flagged that problem immediately, but they never looked at it.

The comparison rate is the right place to start. It is not the right place to finish. I tell every client to treat it as a screening tool. If two loans have similar comparison rates, the next question is what features each loan includes. An adjustable-rate mortgage might show a low comparison rate today but carry rate risk over a longer horizon. A fixed loan with a slightly higher comparison rate may offer more predictability for your budget.

The other thing I see consistently is borrowers who skip the Loan Estimate review because it feels overwhelming. That document is your best protection. It standardizes every fee, shows you the APR, and gives you a direct comparison point across lenders. Bring competing Loan Estimates to each lender conversation. Most lenders will negotiate when they see you have done the work.

Comparison rates give you the first honest look at a loan. Use them, then go deeper.

— David

See how Davidmordue simplifies your mortgage comparison

Understanding comparison rates is the foundation. Taking action on that knowledge is where the real savings happen.

Davidmordue offers fully online mortgage pre-approval and refinance services, with funding possible in under 21 days. You get personalized rate comparisons, expert guidance, and direct access to competitive loan options. Use the Davidmordue rates page to explore current offers and request a pre-approval tailored to your financial goals. For homeowners weighing a refinance, the rent vs. buy calculator helps you model the full cost picture before you commit. Start with the numbers, then let Davidmordue help you act on them.

FAQ

What is the difference between a comparison rate and an interest rate?

The interest rate reflects only the cost of borrowing the loan principal. The comparison rate adds standard fees and charges to that figure, producing a single percentage that more accurately represents the loan's total cost.

Does the comparison rate include all loan fees?

No. The comparison rate excludes optional features like offset accounts, redraw facilities, government charges, and borrower-specific costs. Always request a full Loan Estimate to see every fee itemized.

What is the U.S. equivalent of a comparison rate?

The Annual Percentage Rate (APR) is the U.S. standard equivalent. Lenders are required to disclose APR on all Loan Estimates, and it includes origination fees, mortgage insurance, and discount points alongside the interest rate.

How many lenders should I compare before choosing a mortgage?

The Consumer Financial Protection Bureau recommends comparing at least three Loan Estimates. Research shows that borrowers comparing four quotes saved over $1,200 annually, making the extra effort financially worthwhile.

Can a loan with a higher comparison rate still be the better choice?

Yes. A loan with a higher comparison rate may include valuable features like an offset account or unlimited extra repayments that reduce your effective interest over time. Always weigh features alongside the comparison rate when making your final decision.