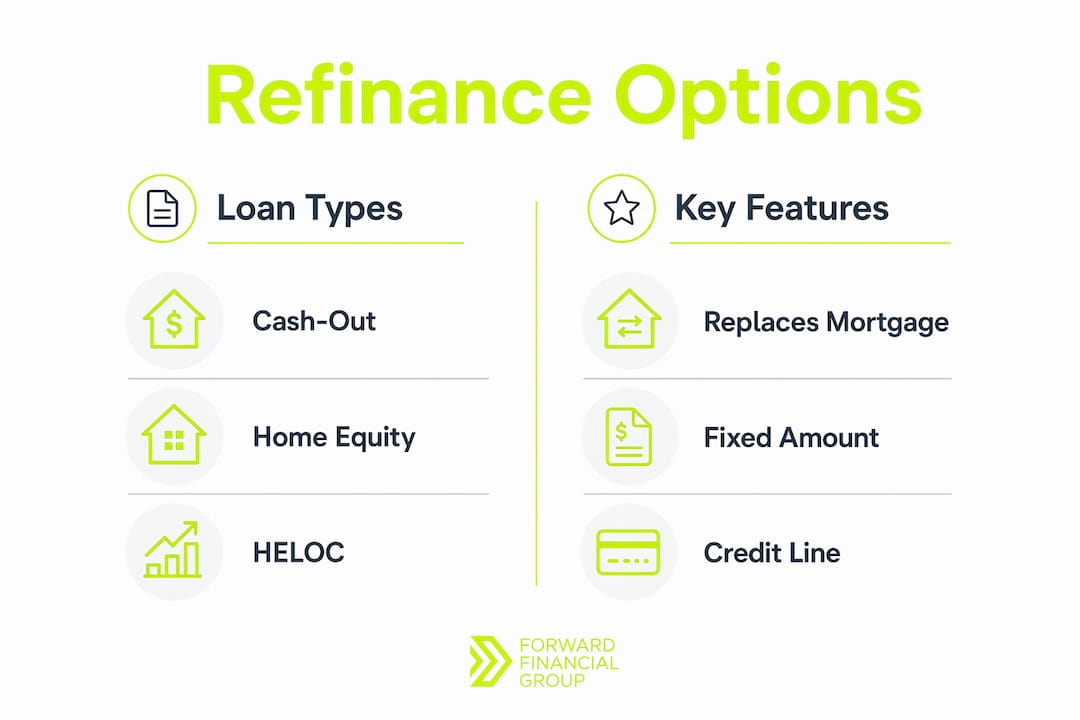

Home equity refinance options are defined as financial products that let you access your home's built-up value, either by replacing your mortgage or adding a second loan. The three main paths are a cash-out refinance, a home equity loan, and a home equity line of credit (HELOC). Home equity loan rates averaged 6.41% as of june 2026, making this a critical moment to compare products carefully. David Mordue - Forward Financial Group works with homeowners every day to match the right product to the right financial goal. The choice you make now affects your monthly payment, your total interest cost, and your financial security for years ahead.

What are the main home equity refinance options?

The three core products work differently, and the differences matter more than most homeowners realize.

A cash-out refinance replaces your existing mortgage with a new, larger loan. You receive the difference in cash at closing. Lenders require 80% max loan-to-value for cash-out refinance qualification, meaning you must keep at least 20% equity in your home. Closing costs run 2%–6% of the loan amount, which can add thousands to your upfront expense.

A home equity loan is a second mortgage. It sits on top of your existing mortgage and delivers a lump sum at a fixed interest rate. You repay it in equal monthly installments over a set term. This product works well when you need a specific amount for a defined purpose, such as a home renovation or debt payoff.

A HELOC (home equity line of credit) functions more like a credit card secured by your home. You draw funds as needed during a draw period, typically 10 years, and repay during a repayment period afterward. Rates are variable, so your payment can rise if market rates increase.

Feature | Cash-Out Refinance | Home Equity Loan | HELOC |

|---|---|---|---|

Replaces existing mortgage | Yes | No | No |

Rate type | Fixed or adjustable | Fixed | Variable |

Disbursement | Lump sum at closing | Lump sum | Revolving credit line |

Typical closing costs | 2%–6% | 2%–5% | Low to none |

Best for | Rate change + cash access | One-time large expense | Ongoing or flexible needs |

Six primary mortgage refinance typesexist beyond these three, including rate-and-term, streamline, no-closing-cost, cash-in, and short refinance. Rate-and-term refinance is the most common choice when your goal is simply to lower your rate or shorten your loan term without pulling cash out.

Pro Tip: If your current mortgage rate is below 5%, financial experts recommend keeping it and adding a HELOC or home equity loan instead of doing a cash-out refinance. Replacing a low rate with a higher one raises your total borrowing cost significantly.

How to evaluate your situation before choosing a refinance path

Your current mortgage rate is the single most important factor in this decision. Maintaining your current mortgage and adding a HELOC may be the better move if your existing rate is historically low. A cash-out refinance that raises your rate from 3.5% to 6.5% on a $400,000 balance adds hundreds of dollars to your monthly payment permanently.

Before you contact any lender, work through these key questions:

How much equity do you have? Most lenders require you to retain 15%–20% after borrowing. Calculate your current loan balance against your home's estimated market value.

What is your credit score? Scores below 680 may limit your options on conventional products. Credit scores below 680 may qualify better for FHA or VA cash-out refinance programs.

What is your borrowing goal? Cash access for renovations, debt consolidation, lower monthly payments, and a shorter loan term each point to a different product.

How long do you plan to stay? Closing costs of 2%–6% can affect break-even; moving within 3–5 years may cancel out any savings from refinancing.

Can you handle a variable payment? A HELOC rate can rise. If your budget is tight, a fixed-rate home equity loan or rate-and-term refinance gives more predictability.

Pro Tip: Ask every lender for a written break-even analysis before you sign anything. This calculation shows exactly how many months it takes for your monthly savings to cover your closing costs. Without it, you are guessing.

Step-by-step process to apply for a home equity refinance

The application process follows a predictable sequence. Knowing each step in advance reduces delays and surprises.

Step | Action | Typical timeline |

|---|---|---|

1. Research lenders | Compare rates, fees, and loan types | 1–2 weeks |

2. Gather documents | Income proof, tax returns, bank statements | 1 week |

3. Submit application | Complete lender's online or paper form | 1–3 days |

4. Home appraisal | Lender orders to confirm value and equity | 1–2 weeks |

5. Underwriting | Lender reviews credit, income, and property | 2–3 weeks |

6. Closing | Sign documents, pay closing costs, receive funds | 1–3 days |

Lenders require an appraisal to confirm your home's current market value before approving any refinance or home equity loan. The appraisal directly determines how much equity you can access. A low appraisal can reduce your borrowing limit or disqualify you entirely.

For borrowers with FHA, VA, or USDA loans, streamline refinance options reduce paperwork and may not require a new credit check or appraisal. This speeds up approval significantly. Veterans and active-duty military members can explore VA refinance options that are not available to the general public. Borrowers with lower credit scores should review FHA cash-out programs as a more accessible path.

Pro Tip: Pull your credit report at least 60 days before applying. Dispute any errors and pay down revolving balances to below 30% of your credit limits. These two steps alone can raise your score enough to qualify for a better rate tier.

Common mistakes homeowners make when refinancing equity

Most refinancing regrets come from the same handful of errors. Recognizing them before you commit saves real money.

Ignoring closing costs. A refinance that saves $150 per month but costs $9,000 in closing costs takes 60 months to break even. If you sell in year four, you lost money.

Replacing a low-rate mortgage unnecessarily. A cash-out refinance may raise long-term borrowing costs if your original mortgage rate is very low. Adding a second loan often costs less overall.

Overborrowing. Pulling out more equity than you need increases your debt load and your monthly payment. Borrow only what the specific goal requires.

Confusing a home equity loan with a HELOC. A home equity loan gives you one fixed payment. A HELOC gives you flexibility but variable costs. Choosing the wrong one for your situation creates payment stress.

Not shopping multiple lenders. Rate differences of even 0.5% on a $200,000 loan add up to thousands of dollars over the life of the loan. Get at least three quotes.

"The most expensive refinance mistake I see is homeowners who cash out equity to consolidate debt, then run the credit cards back up. The refinance doubled their problem. Treat a cash-out refinance as a one-time financial reset, not a recurring solution."

Key Takeaways

The right home equity refinance option depends on your current mortgage rate, your equity level, your credit score, and how long you plan to stay in the home.

Point | Details |

|---|---|

Match product to goal | Cash-out refinance suits rate changes plus cash needs; home equity loans suit fixed expenses; HELOCs suit flexible needs. |

Protect your low rate | Keep a sub-5% mortgage and add a HELOC or home equity loan rather than replacing it with a higher rate. |

Calculate break-even first | Closing costs of 2%–6% mean you need years of savings to justify refinancing; always get a break-even analysis. |

Credit score shapes options | Scores below 680 open FHA or VA pathways; improving your score before applying saves money on rates. |

Appraisal determines access | Your home's appraised value sets your borrowing limit; a low appraisal can reduce or block your loan. |

What I have learned about choosing the right equity strategy

After working with homeowners across a wide range of financial situations, the pattern I see most often is this: people focus on the monthly payment and ignore the total cost. A lower payment sounds like a win. But if you extended your loan term by 10 years to get it, you paid far more in interest over time.

The second thing I have learned is that timing matters more than most people admit. Homeowners who refinanced in 2020 and 2021 locked in rates below 3.5%. Many of them are now sitting on significant equity but are reluctant to touch it because a cash-out refinance would replace that rate. That instinct is correct. A HELOC or home equity loan preserves the original mortgage and still gives access to equity. That is the right call for most of those borrowers right now.

The third lesson is about goals. Refinancing for a home improvement project that adds real value to the property is a sound use of equity. Refinancing to fund a vacation or cover recurring expenses is not. The home is collateral. Every dollar you borrow against it carries real risk if your income changes.

My advice is to treat refinancing as a financial tool with a specific job, not a general solution to cash flow problems. Define the goal first. Then find the product that fits the goal at the lowest total cost. David Mordue - Forward Financial Group helps homeowners run those numbers honestly, without pressure, so the decision is clear before any application is submitted.

— David Mordue

How David Mordue - Forward Financial Group supports your refinance decision

Choosing between a cash-out refinance, a home equity loan, and a HELOC is easier when you have real numbers in front of you. David Mordue - Forward Financial Group offers personalized consultations and rate comparisons built around your specific equity position, credit profile, and financial goals.

Use the refinance calculator to model your break-even point and compare monthly payment scenarios across different loan types. When you are ready to move forward, the mortgage pre-approval process at David Mordue - Forward Financial Group is fully online and can reach funding in less than 21 days. Check current refinance rates to see where the market stands today before you commit to any product.

FAQ

What is the difference between a cash-out refinance and a home equity loan?

A cash-out refinance replaces your existing mortgage with a larger loan, while a home equity loan adds a second mortgage on top of your current one. The key difference is that a cash-out refinance changes your primary mortgage rate and term.

How much equity do I need to qualify for a cash-out refinance?

Most lenders require you to retain at least 20% equity after the loan closes, meaning the maximum loan-to-value ratio is 80%. Your home's appraised value determines how much you can borrow.

Should I choose a HELOC or a home equity loan?

Choose a home equity loan when you need a fixed amount for a one-time expense and want predictable payments. Choose a HELOC when your cash needs are ongoing or uncertain, and you can manage a variable interest rate.

What credit score do I need to refinance home equity?

Conventional cash-out refinance typically requires a minimum credit score of 620. Borrowers with scores below 680 often find better terms through FHA or VA cash-out refinance programs.

How long does a home equity refinance take to close?

A standard refinance takes 30–45 days from application to closing, depending on appraisal scheduling and underwriting volume. Streamline refinance programs for FHA, VA, and USDA borrowers can close faster due to reduced documentation requirements.